I writing a topical email every week to my mailing list. Here’s our last email to subscribers which I thought I share.

Q4 hedge fund letters, conference, scoops etc

You can sign up on our mailing list to get the latest updates when it goes out every week.

Investing for “yield” is one of the main draws of the Singapore stock exchange.

However, investors chasing yield have been burn badly in recent years – something I have talked about.

The following email will cover both dividend paying stocks, bonds, preference shares and perpetuals.

This email is one of the longest emails I’ve sent out but bear with me as the lessons here are timeless and apply to almost any investing situation.

In this article, I am going to run through how investors can analyze whether a company’s dividend or payout is sustainable in the long run using simplified financial ratios.

Understanding how the company actually makes money

First off, it goes without saying that it is important that investors must understand the business model of the company first.

For example, there is a very big difference in investing in a telco that is still building its infrastructure (aka TPG Telcom’s Singapore Operations) and not generating revenue yet vs an already established telco that already has pre-existing cash flow.

For property development, you normally experience significant cash outflow in the earlier years as the property is being built, and significant cash inflows later on as the property is completed and handed over to the end user.

This understanding of different business models is absolutely critical because the gap between cash outflows and inflows has to be funded either by debt or equity.

If a company does not have enough cash or recurring revenue on hand to meet its short-term liabilities, it will spark a liquidity crisis.

A property development company that has its sole activity as property development and a property development company with a significant amount of investment properties generating recurring revenue are completely different beasts.

One has significant recurring income and monetizable assets that can tide it through disruptions (for example construction accidents). The other does not.

Each business model has their own pros and cons.

Having a strong sponsor / majority shareholder is often the critical element in my assessment of business models which require huge amounts of capital upfront with payback only coming in subsequent years.

Singtel, Starhub and Hyflux & Free Cash Flow Analysis

After understanding the business model, investors must look to the free cash flow generation ability of the company in question. I am going to use the case studies of Singtel, Starhub and Hyflux to drive home the importance of this.

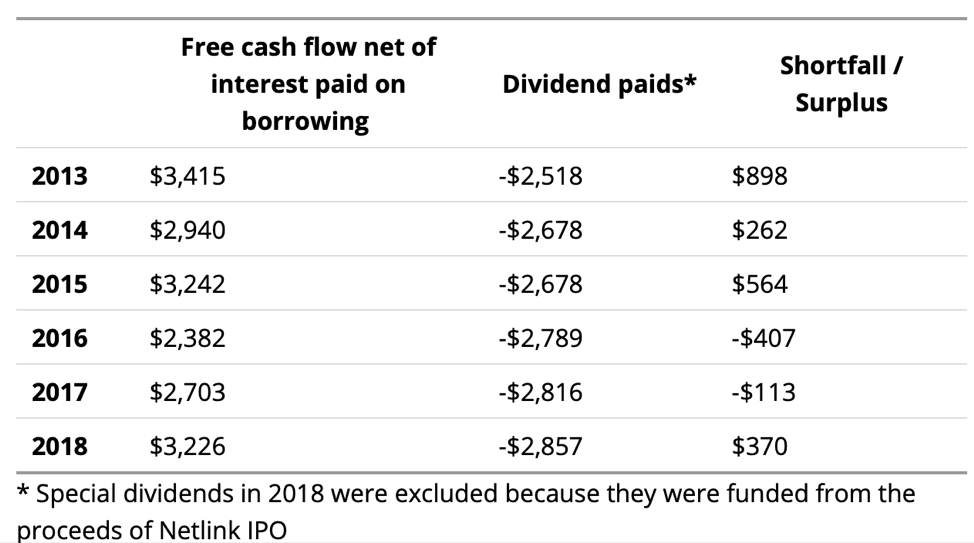

In the case of Singtel, its businesses have come under multifold pressure from its core operations in Singapore to its overseas operations in India and Indonesia.

At the same time, its core dividend has not been cut. In fact, it paid out a special dividend in 2018 from the proceeds from the IPO of Netlink Trust.

Quite simply, it was generating free cash flow in excess of its dividend payout.

Of the three stocks we talk about, its share price has corrected the least, falling about 30%+ in the last few years from peak to bottom.

It is important to note that while investors are concerned about its outlook, questions regarding its dividend payout and financial strength are not a major issue today.

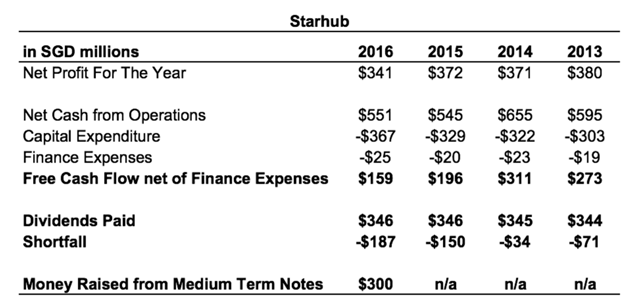

The same cannot be said for Starhub which has its operations focused in Singapore. Starhub was a widely held “yield stock”.

Unfortunately, Starhub was paying out more in dividends then free cash flow generated.

As a result, when its business operations begun to suffer from the ensuing price war, it was forced to cut its dividend several times to reflect the new business reality.

Starhub’s price has fallen more than 60% over the last few years from peak to bottom.

It is important to note that are both concerned about its outlook and its ability to sustain its dividend payout given its current challenges.

The most troubled of the three companies cited is Hyflux.

The woes that beset Hyflux have been well covered by the media and this blog in previous posts.

It is currently under severe distress. What I want to draw your attention to is that even in prior years, Hyflux was experiencing hugely negative free cash outflows.

Source: FT.com

The cash flow gap had to be funded from equity and debt fund raises. Debt and its related securities eventually come due and rolling it over is never guaranteed.

Unfortunately, Hyflux ran out of time.

Shareholders today are facing a virtual wipeout. Investors in its perpetual securities and preferences are looking at recovery rates of barely 10 cents on the dollar.

Needless to say, permeant capital losses vastly exceeds that of both Starhub and Singtel as they will be crystallized post restructuring.

Margin of Safety

When Graham was confronted with the challenge to distill the secret of sound investment into three words, he ventured the motto, MARGIN OF SAFETY.

He stated that it was the common thread that ran through his entire investment philosophy.

I am in full agreement with Graham on this and I hope that the following article has reflected the same underlying principle.

To summarize, investors must always take a three-fold step when assessing sustainable dividend or interest payouts.

- Assessing and understanding the basics of the business model of the company

- Analyzing whether the company is generating enough free cash flow to cover the payouts

- Demanding a margin of safety to consider downturns and business declines (i.e. company must be generating excess free cash flow to fund these payouts)

Simply put, if you were an engineer building a bridge, you would first ask yourself what the expected weight the bridge is required to bear.

Assuming that you think that it would have a maximum of 500kg of weight at any one time, you would still want to impute a “margin of safety” – allowing it to bear at least 750kg of weight in the event that you are wrong.

Taking to the same concept to stocks and fixed income securities is easy enough.

Assuming that the company is paying out a 60 cent dividend, you want it to be generating cash in excess of 90 cents to give you a margin of safety.

Ending thoughts:

In the above analysis, I have not dug into the Annual report but relied on simplified financial ratios easily obtainable online.

Successful investing over the long run requires at least basic fundamental analysis and investors can only rely on themselves to protect their capital.

Regards,

Richard Tay (Jun Hao)

Article by The Asia Report