Fundraising for these real estate vehicles is lacklustre as the industry awaits final regulatory guidelines from the US Treasury

Q3 2019 hedge fund letters, conferences and more

Opportunity Zone Funds (OZFs) are designed to enable investors to do well by doing good. Created to spur investment in low-income communities designated as ‘Opportunity Zones’ by the US Government, OZFs have champions in high places. Tech entrepreneur and philanthropist Sean Parker – who co-founded music sharing service Napster and later became Facebook’s first President – helped to drive the initiative to create these Zones. OZFs have the potential to become “its own asset class, and it could be a very large asset class,” Parker told the New York Times in an interview last year. But sparking investor interest in a new asset class has not been easy.

Opportunity Zones arose as part of the Tax Cuts and Jobs Act of 2017, and today they span all 50 states, the District of Columbia, and the five US territories. To attract investment, OZFs offer investors significant deferrals on their capital gains taxes. By channelling the gains from an asset sale into an OZF and retaining their interest in the fund for at least 10 years, investors are exempt from paying capital gains taxes on any rise in the value of their OZF investment. But so far, take up has been slow.

Back in January 2019, when Preqin surveyed investors to gauge their interest in OZFs, 92% of respondents said they were currently not invested in OZFs, citing regulatory uncertainty and the risks of investing in distressed areas. Fast-forward to today, and investor demand remains sluggish.

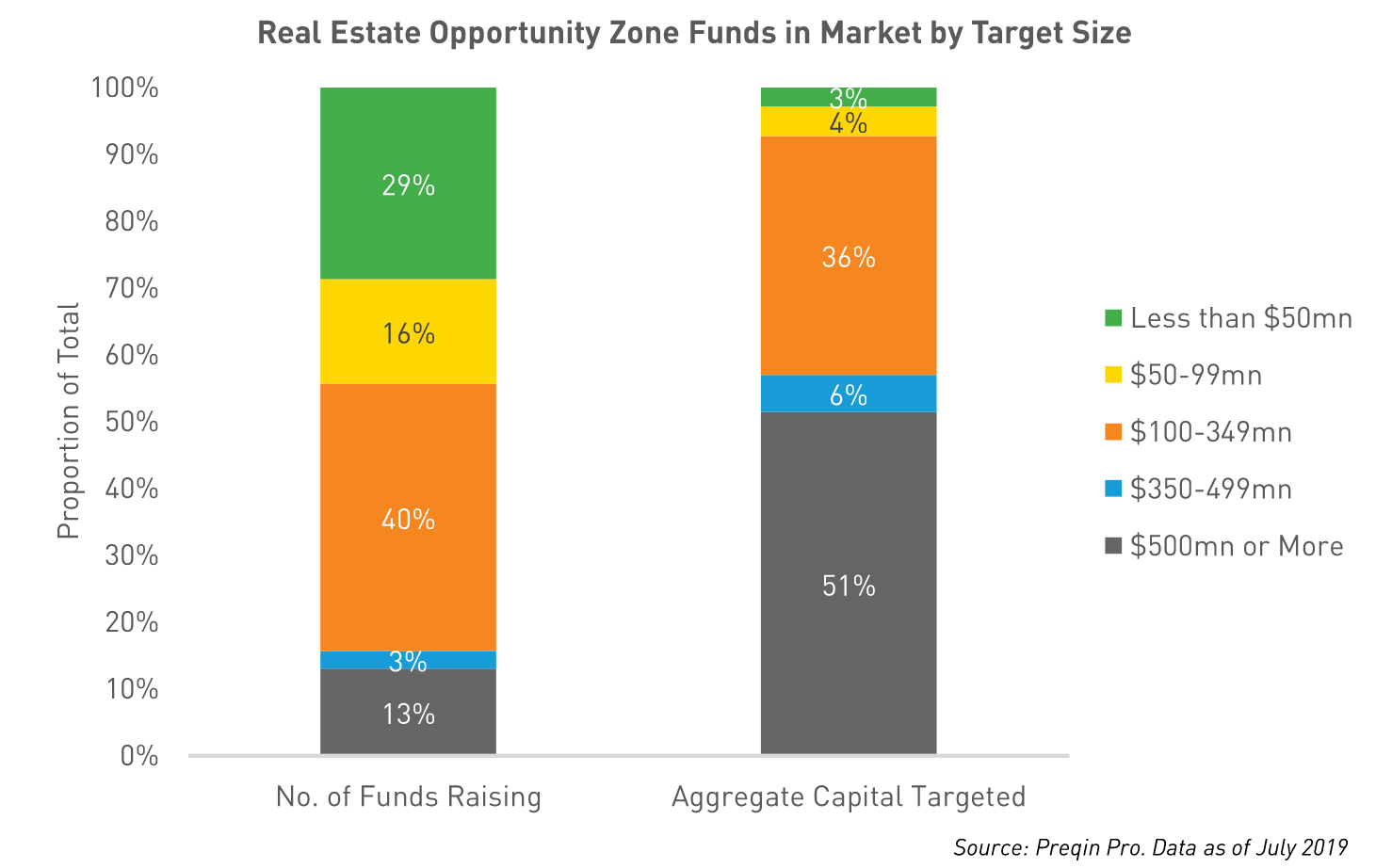

A Slow Start to Fundraising Opportunity Zone Funds

Consider the fundraising figures for OZFs. Right now there are 151 closed-end OZFs in market, a small fraction of the 7,400+ private real estate funds listed on Preqin Pro. Of these 151 funds, just 18 have held a final close, accounting for $2.3bn in commitments. Moreover, $755mn of that capital is committed to just one GP, Federal Capital Partners, whose FCP Realty Fund IV targets value-added investments in the US. The remaining 133 OZFs are targeting a total of $20bn in capital, with only 24% having held at minimum a first close. That means the majority of OZFs now in market have yet to secure significant investor capital.

Investor Demand for Opportunity Zone Funds Will Come Down to Performance

A major reason for the slow uptake of OZFs is the lack of regulatory clarity. In January 2018, shortly after the tax cut that gave rise to OZFs was enacted, the US Government shut down. Fund managers that were just getting started with OZFs had to wait for further guidance, and the long delays put off potential investors. While part two of the regulations is now available, fund managers are still awaiting the final guidelines, which are slated to be released later this year.

Since the regulatory framework has yet to be fully clarified, there are currently only a small number of established firms that have set up OZFs. Indeed, nearly 70% of the OZFs in market are first-time funds. Their struggle to gain traction mirrors the broader trend seen in the private real estate market: these days larger, more established managers are attracting the lion’s share of investor capital, crowding out emerging managers. Industry participants say there are plenty of Opportunity Zone deals to be made, but the supply of capital is limited since the fundraising pace has been slower than expected.

Another complication is the way OZFs are structured. OZFs are designed to encourage long-term investment of at least 10 years to realize their full benefit. Their performance J-curve is expected to be ‘low and long’ compared with typical private real estate funds, which means investors have to wait longer for distributions.

There are some bright spots, of course. Since 2018, five funds have successfully raised more than $100mn.1 That is less than a third of the 18 OZFs that have closed, but it is still early days for OZFs. Plus, as the end of the tax year approaches, investors will be assessing their portfolios and fund managers will be hoping that some of their capital gains will be diverted into their OZFs. A number of OZFs are known to be targeting net IRRs in the high teens to the low twenties, an attractive long-term return for investors on the hunt for yield. If returns are as strong as targeted, investors may well decide that there is money to be made in doing good after all.

For more information on OZFs, read our factsheet which further examines investors’ plans for OZFs.

1Other than Federal Capital Partners’ FCP Realty Fund IV, which closed in October 2018, these are:

- Sugar Hill Capital Partners’ $130mn value-added fund, closed in December 2018

- Starwood Capital Group’s $304mn opportunistic fund, closed in January 2019

- BlackSand Capital’s $327mn opportunistic fund, closed in April 2019

- Bridge Investment Group’s $509mn value-added fund, closed in July 2019

Article by Justin Bartzsch, Preqin