RPD Fortress Fund’s commentary for the month ended June 30, 2025.

Read more hedge fund letters here

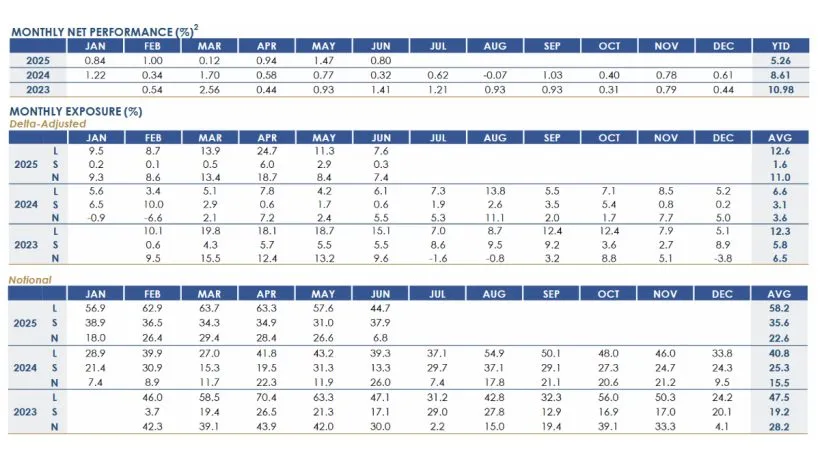

RPD Fortress Fund returned +0.80% net in June, bringing year-to-date net performance to +5.26%. The Fund has now delivered positive returns in 28 of the past 29 months, continuing to demonstrate consistency across a range of market environments, achieved without the use of any leverage.

The estimated performance figures net of fees as of June 30, 2025

| Month | Year to Date | Inception to Date* | |

|---|---|---|---|

| RPD Fortress Fund | 0.80% | 5.26% | 26.88% |

| BarclayHedge Equity Long Short Index** | 1.43% | 4.80% | 19.79% |

| US High Yield Corporate Bond Index | 1.84% | 4.93% | 23.24% |

Performance Statistics

| CAGR | Volatility | Sharpe | Positive Months |

|---|---|---|---|

| 10.35% | 1.83% | 3.41 | 97% |

Both put and call selling contributed positively in June. A notable example was Abercrombie & Fitch (NYSE:ANF), which reported strong earnings. The stock reacted positively in June, and our strike selection—anchored to valuation levels we considered especially conservative—allowed us to benefit meaningfully. Performance was broad-based across sectors including consumer discretionary, software, semiconductors, AI infrastructure, retail and apparel, e-commerce and marketplaces, telecom and IT services, and gaming and leisure. As always, all options sold were fully cash-secured, with significant buffers between strikes and underlying prices.

While the recent rally has made it more difficult to identify new opportunities that meet our valuation and risk/reward thresholds, we continue to observe macro uncertainty and stretched valuations in parts of the market. As such, we remain patient and selective, while ready and prepared to act decisively should volatility increase or dislocations emerge.

Average notional exposure in June was 44.7% long and 37.9% short, resulting in gross exposure of 82.6% and net of 6.8%. On a delta-adjusted basis, exposure averaged 7.6% long and 0.3% short, or 7.9% gross and 7.4% net. As of June 30, current notional exposure stands at 47.3% long and 35.8% short (gross 83.1%, net 11.5%), with delta-adjusted net exposure of 9.2%.

Reminder: Beginning September 1, 2025, redemption terms for new investments will change from monthly with 45 days’ notice to quarterly with 30 days’ notice. Liquidity at the portfolio level remains unchanged; this adjustment is intended solely to enhance long-term alignment and support portfolio stability. All investments made prior to September 1 will retain current redemption terms.

If you have any questions or require additional information, please contact Investor Relations at [email protected].

Best regards,

RPD Fund Management LLC