Greg Lippman’s LibreMax Partners outperformed the broader markets in the first quarter, returning 2.97% for the first three months of the year. The S&P 500 Total Return Index was off 4.27% for Q1, while the HFRI Fund Weighted Composite Index was down 0.42%. The HFRI RV Fixed Income Asset Baked Index gained 2.27%, and the Merrill Lynch High Yield Cash Pay Index was up 0.97%.

Read more hedge fund letters here

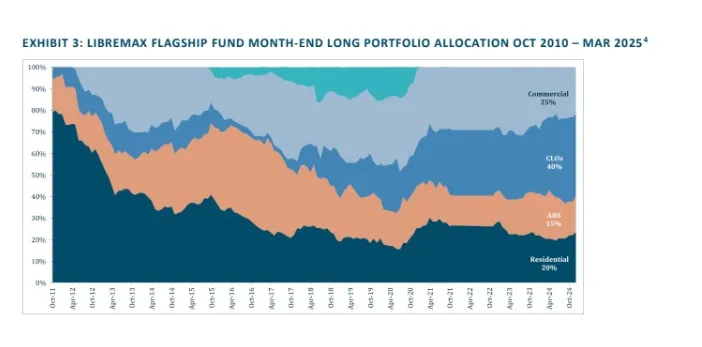

LibreMax had about $11.8 billion in assets under management at the end of March.

Lippmann, whose massive short of subordinated tranches of residential mortgage-backed securities at the beginning of the Great Financial Crisis was chronicled in The Big Short, reported that disciplined hedging and active repositioning enabled them to generate positive returns in every months of Q1.

Also see The ‘Accidental’ Phone Call Which Started It All: Interview With The Big Short’s Danny Moses

Market environment

In his Q1 letter to investors, which was obtained by Hedge Fund Alpha, Lippmann noted that U.S. equities continued to capture a larger share of global allocations going into 2025. In particular, U.S. equities were taking share from Europe, where expectations for growth were lower.

However, by the end of the first quarter, European equities were soaring, representing a major turnaround in the markets. The U.S. markets underperformed compared to their global peers while yields diverged.

In the U.S. economic reports started to show early signs of trouble as consumer spending declined and corporate earnings forecasts were slashed. Meanwhile, inflation rose and policy uncertainties surfaced. Volatility spiked and asset classes repriced amid some major developments, including disruption from Deepseek, renewed threats of tariffs from President Donald Trump, and Germany’s turnabout in fiscal policy.

Lippmann believes the current environment underlines the importance of key parts of their philosophy, including flexibility, risk management and a focus on dislocation-driven opportunities.

Asset-backed securities

New issue volume for ABS hit its third-highest supply ever recorded during Q1, with autos and esoteric assets like data centers, whole business and fiber leading the way. Macro volatility resulted in weaker subscription levels, so LibreMax selectively boosted its exposure to traditional auto, consumer unsecured and fiber deals as the environment enabled it to provide liquidity.