Executive Summary

In the last eight months, investor flows to hedge funds have been positive only once, but that does not mean funds are not gaining new assets. If you’re a large firm that performed well in 2018, chances are 2019 is feeling like a very positive year. For large firms that under-performed in 2018, then 2019 is likely feeling very different.

Q1 hedge fund letters, conference, scoops etc

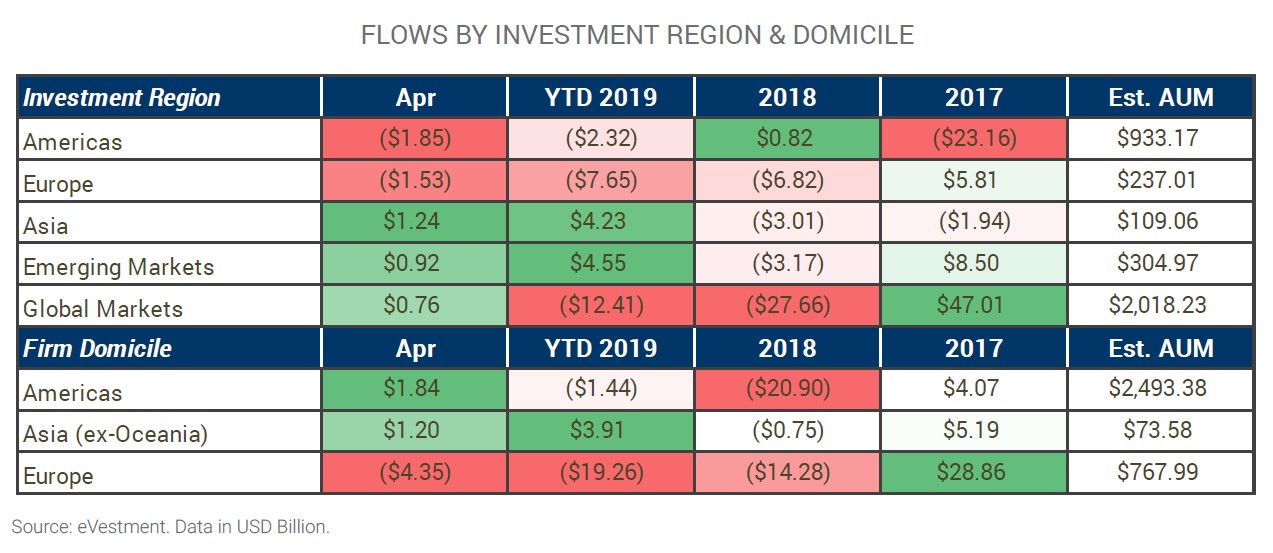

We have been persistently noting that the current state of flows appears to be less of a “hedge fund industry” issue and more of a performance issue. Look no further than Europe, where the bulk of the seemingly large redemption pressures are coming from a subset which was unable to produce one product with attractive returns last year.

To date, 2019 has been a much more positive performance environment for managers, however it has been positive for most asset classes, and so the competition for assets will continue to be difficult.

Highlights

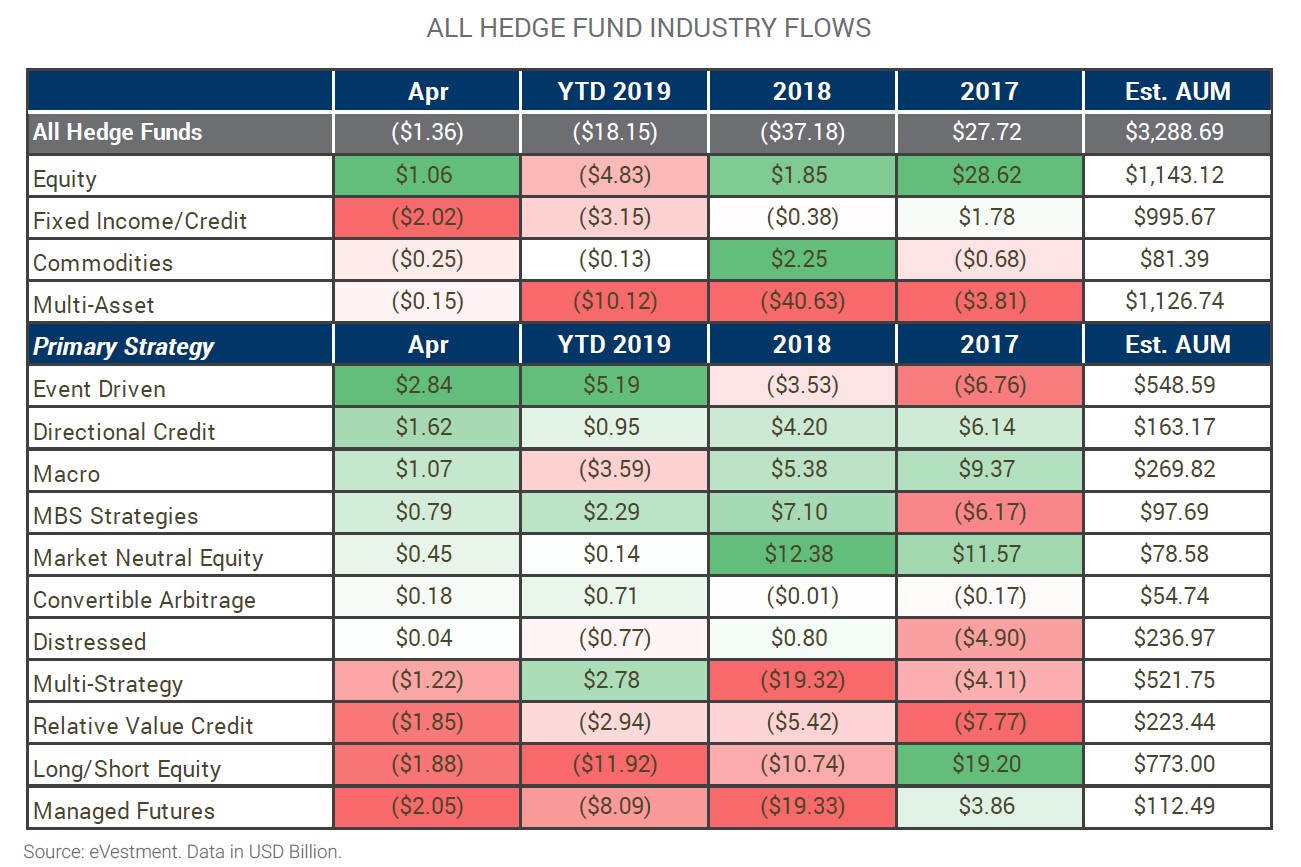

- Investors redeemed an estimated $1.36 billion from hedge funds in April. YTD redemptions are now $18.15 billion.

- There has been targeted interest in event driven strategies in 2019, highlighted by elevated inflows in April.

- Macro fund flows shifted to positive in April, pausing a trend of redemption pressures dating back to September 2018.

- EM hedge funds had inflows again in April. Allocations continue to be directed toward China-focused strategies.

Aggregate Flows Flat in April, Though Active at Strategy Level

Investors redeemed an estimated $1.36 billion from hedge funds in April 2019, bringing YTD flows to a negative $18.15 billion. Performance was again additive to total industry AUM, which sits at $3.289 trillion.

Don’t let the flat flows fool you, there was plenty of investor activity in April.

Yes, in the last eight months, investor flows to hedge funds have been positive only once, but that does not mean funds are not gaining new assets. Given that flows were nearly flat during the month (the norm rather than exception over the last four Aprils), it also means funds are continuing to lose assets as well.

Just over 56% of reporting managers had outflows during the month, which is below the level in March, but above the monthly average of the last three years.

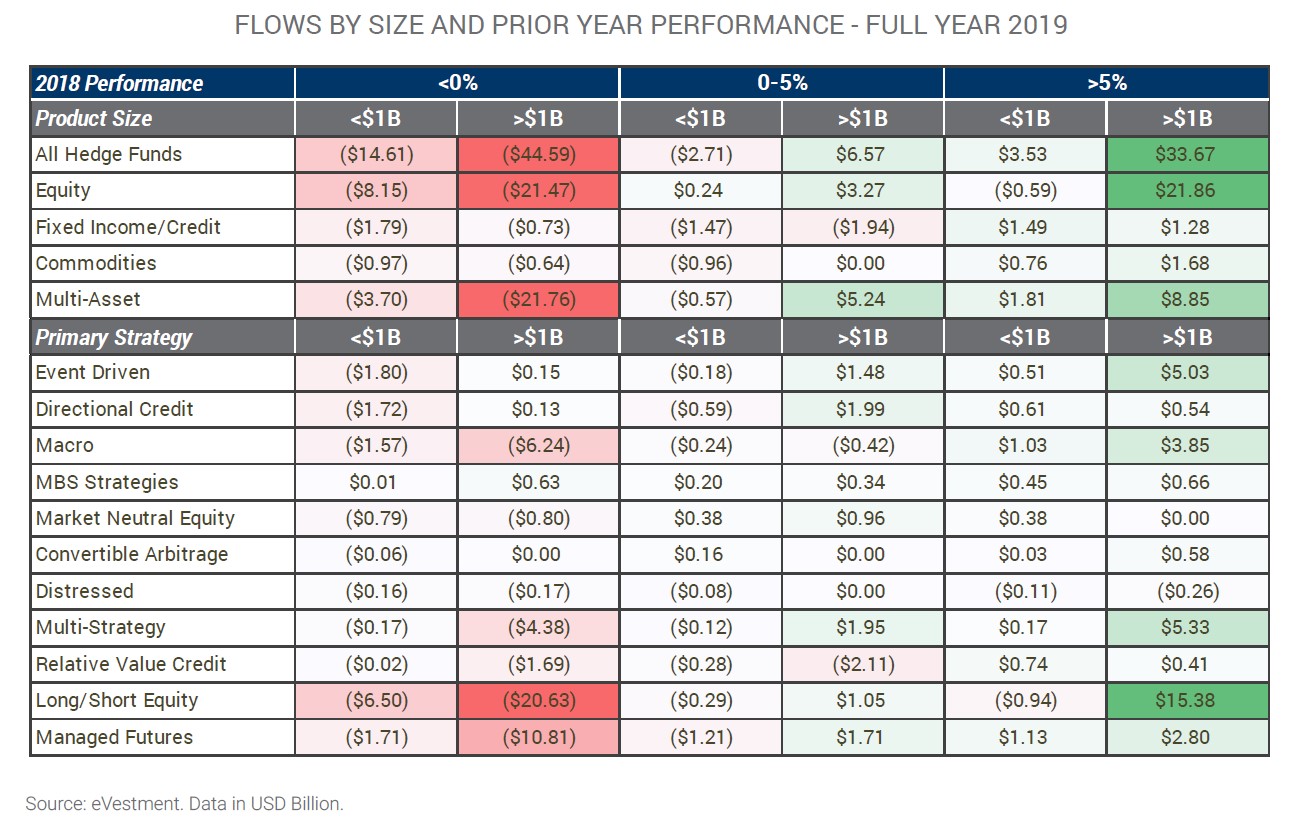

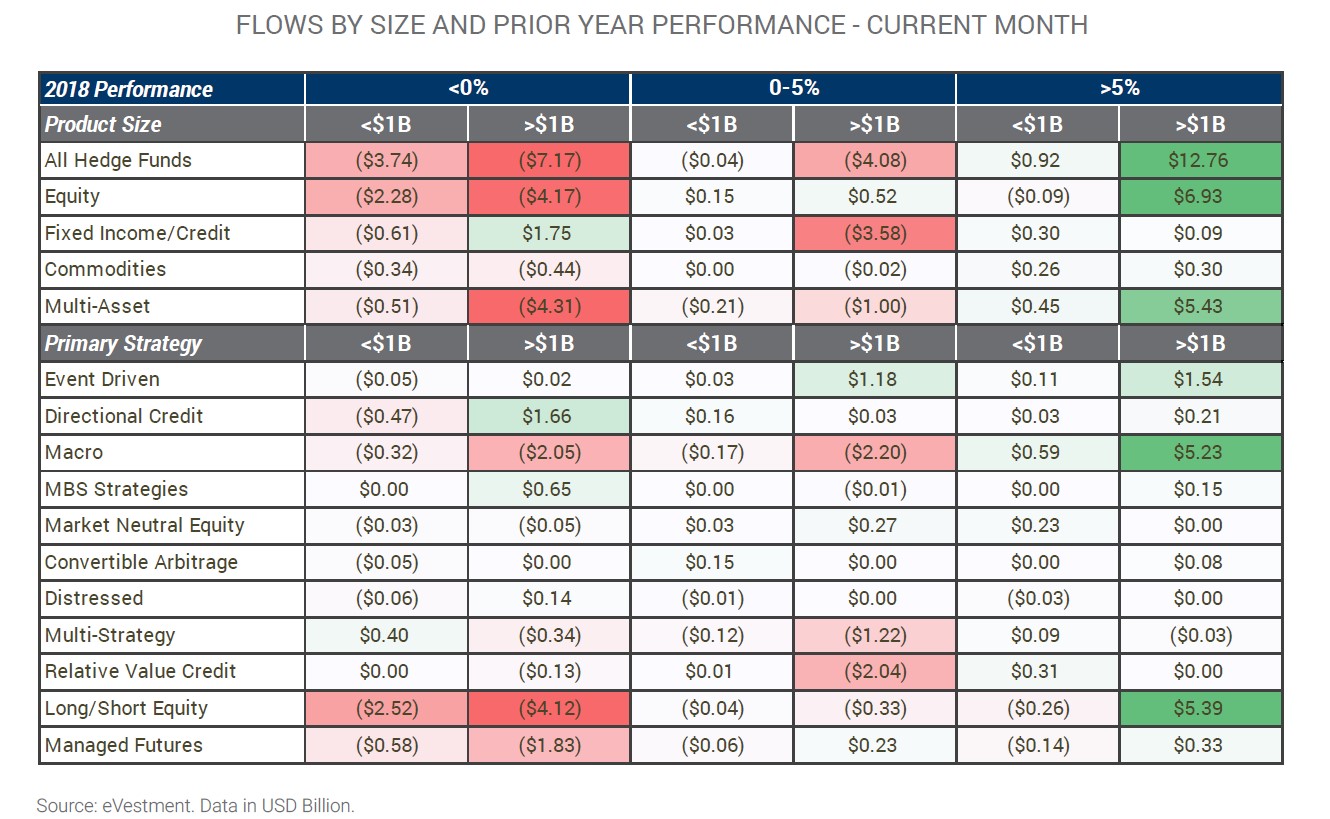

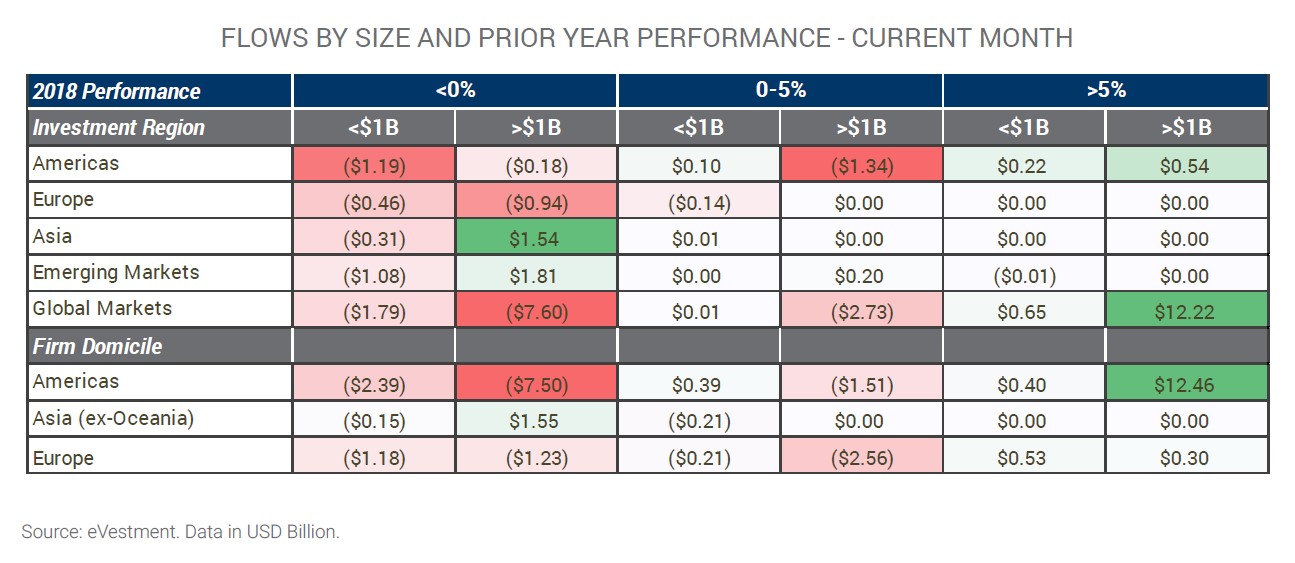

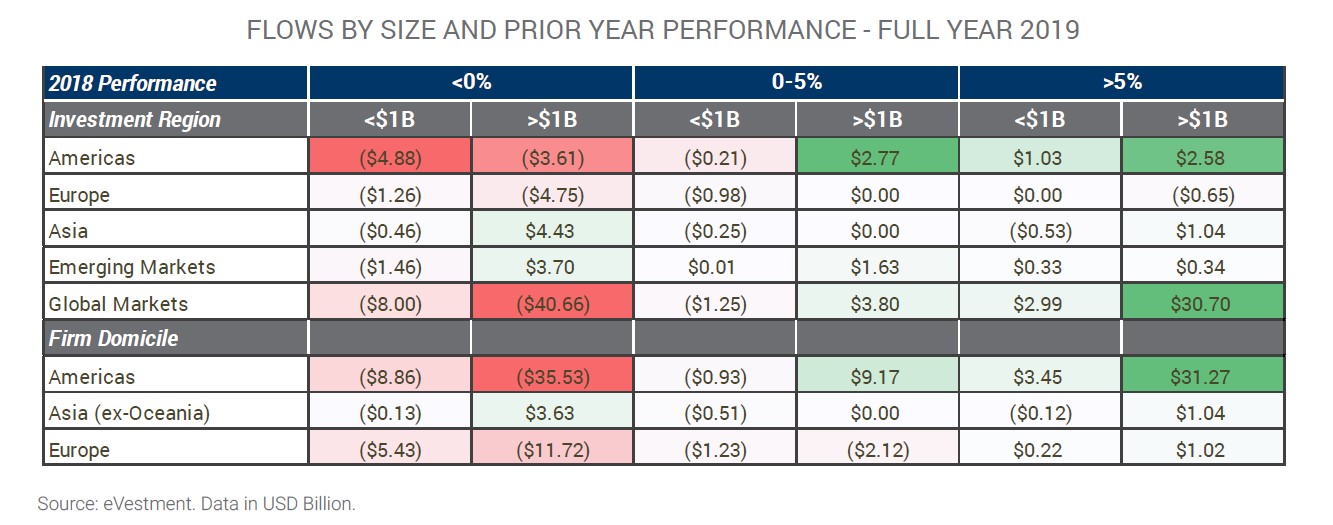

Prior year returns continue to meaningfully influence 2019 flows.

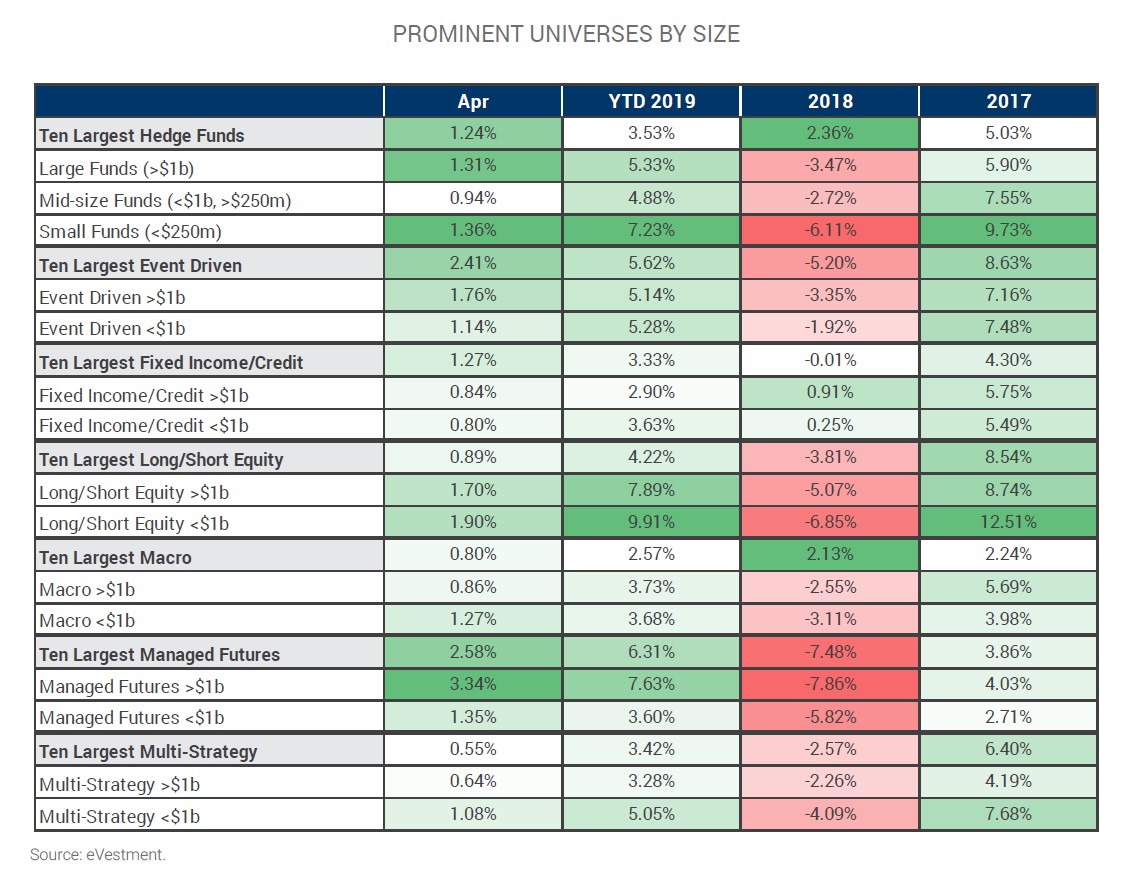

If you’re a large firm that performed well in 2018, chances are 2019 is feeling like a very positive year. For large firms that underperformed in 2018, then 2019 is likely feeling very different. The segments where this theme is most noticeable is within macro and long/short equity strategies.

Investors show interest in event driven strategies to start Q2 2019.

There were a few larger targeted allocations within the event driven segment in April which helped lift the strategy’s profile during the month.

Even though allocations were targeted, 56% of reporting ED funds had inflows in April and there were no large redemption pressures evident. With $5.19 billion of inflows YTD, event driven strategies have seen the most net new money in 2019 among primary strategies.

Macro flows turned positive after a string of redemptions.

After elevated losses in July/August 2018, there have been lingering redemption pressures facing macro funds. Prior to April, monthly flows have been negative in six of the last seven months with an estimated $13 billion removed. April’s inflow of $1.07 billion is a welcome shift to positive, and it was driven by the $5.23 billion of inflows to funds able to perform well in 2018.

Managed futures funds continue to feel redemption pressure.

April marks the fourteenth consecutive month where managed futures funds have had net outflows. The spark for this difficult stretch appears to be large losses in February 2018. Since then there has been two other noticeable drawdowns, but most recently performance has been very positive. The next few months will be of interest to see if there is new appetite for the products. There is an extended period of adverse performance which must be addressed, but recent returns will do nothing except help the strategy’s cause.

Demand for hedge funds exists within U.S. public plans.

A point we made last month is worth reiterating. Outside of our calculated asset flow data, eVestment sees pockets of demand from U.S. pension plans via documents in our MarketLens solution. In a report to be released shortly, we note that in aggregate U.S. public plans are slightly below target HF allocations, which implies a level of demand to move current allocations in-line with targets.

Emerging Markets Continue to See Targeted Inflows

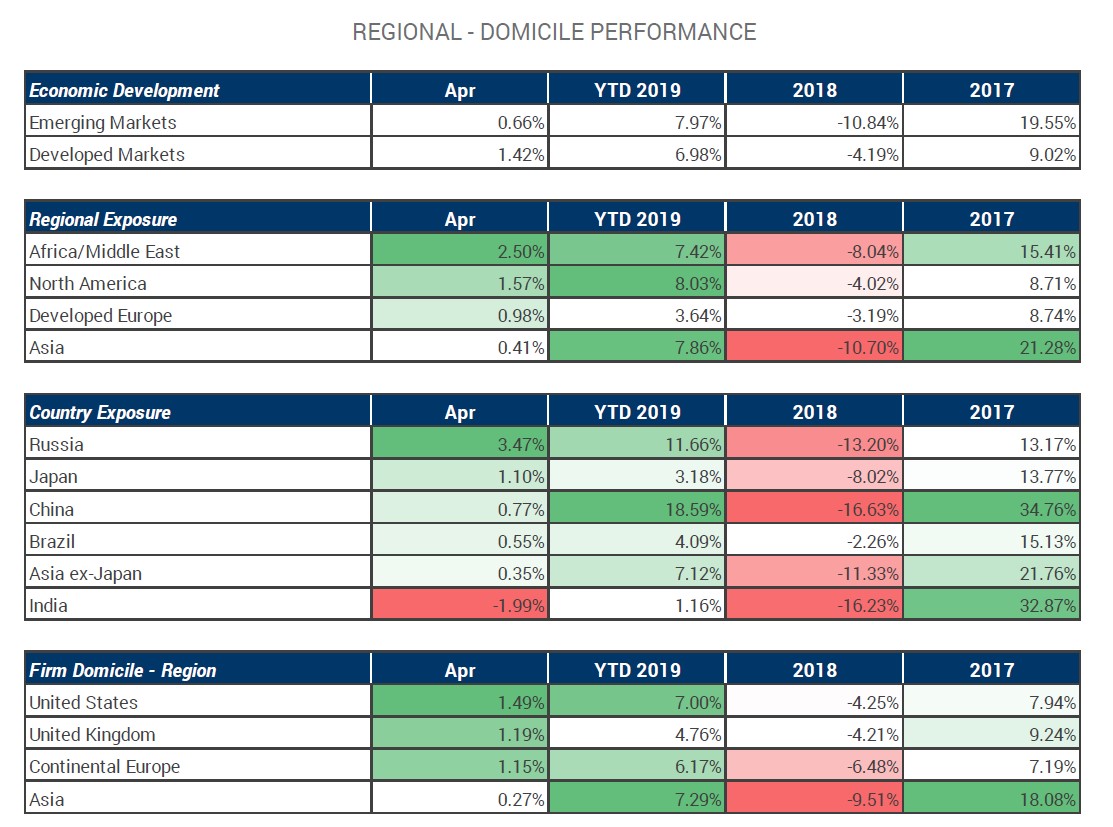

April was positive for EM strategies with flows again targeted to China.

As EM hedge funds as a universe were receiving net inflows in Q1, we noted allocations were not widespread across the group. This theme continued into April, the result being that it appears like EM strategies are in high demand, but the data shows only 26% of reporting managers have had inflows YTD. The bulk of the assets have gone to China-focused funds, with preferences toward fixed income strategies.

European managers continue to see assets leave in 2019.

First, this is not a universal issue in Europe. There are managers able to raise capital both in the UK and continental Europe. It is likely not a coincidence, however, that of the ten funds with the largest YTD 2019 redemptions, not one had a return over 5% in 2018, and average returns for that group last year were -0.67%.

The average U.S. domiciled fund returned -4.25% in 2018 compared to the average from continental Europe of -6.48%, and the average among the ten largest funds overall was +2.36%. The European hedge fund space is suffering in 2019, but blaming BREXIT does not address another key issue, which is poor performance. Again, this is not a universal problem for this segment, but simply a very noticeable one.

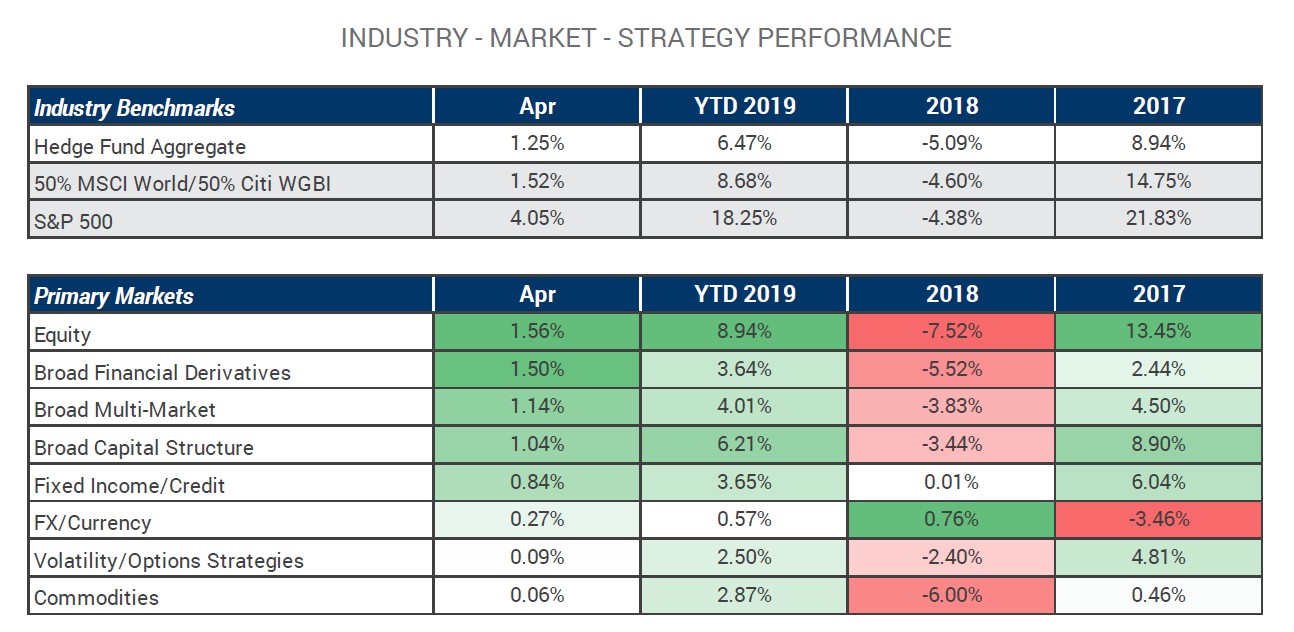

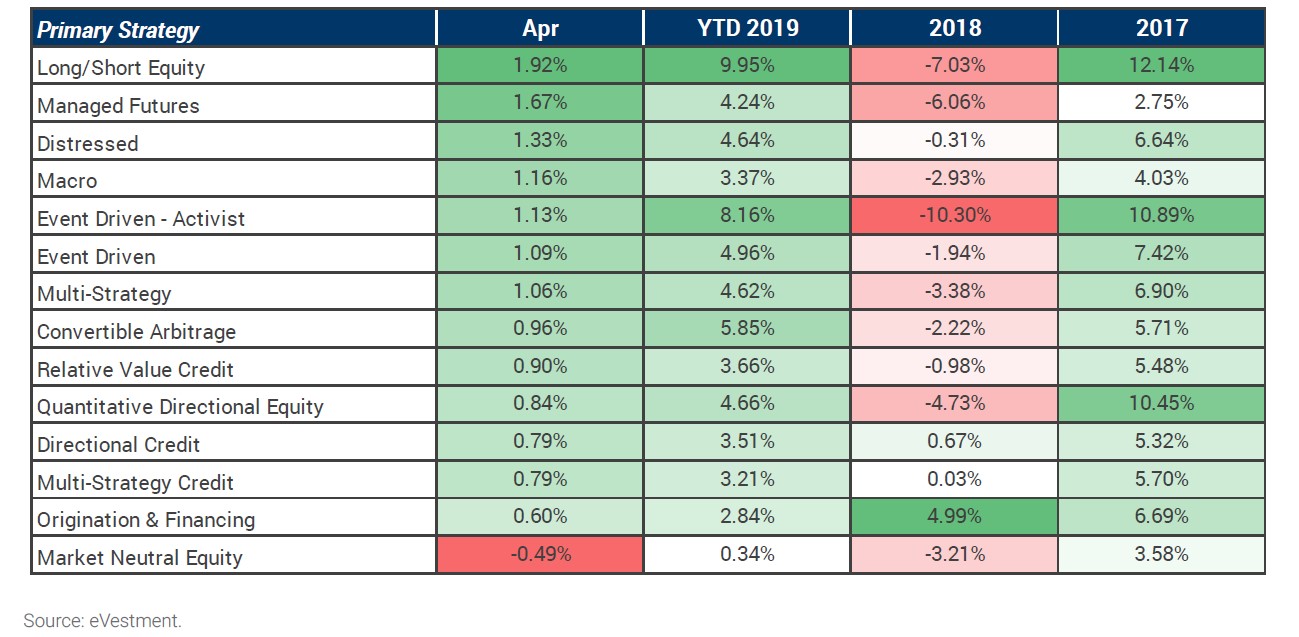

Hedge Fund Performance Tables

Article by Preqin