Tyler Cowen recently linked to a study of China’s economic growth, which suggests that official figures (roughly eight percent) overstate the real GDP growth rate by about 1.8 percent/year between 2010 and 2016:

Q1 hedge fund letters, conference, scoops etc

Using publicly available data, we provide revised estimates of local and national GDP by re-estimating output of industrial, construction, wholesale and retail firms using data on value-added taxes. We also use several local economic indicators that are less likely to be manipulated by local governments to estimate local and aggregate GDP.

The estimates also suggest that the adjustments by the NBS were insufficient after 2008. Relative to the official numbers, we estimate that GDP growth from 2010-2016 is 1.8 percentage points lower and the investment and savings rate in 2016 is 7 percentage points lower.

Low Error Rate

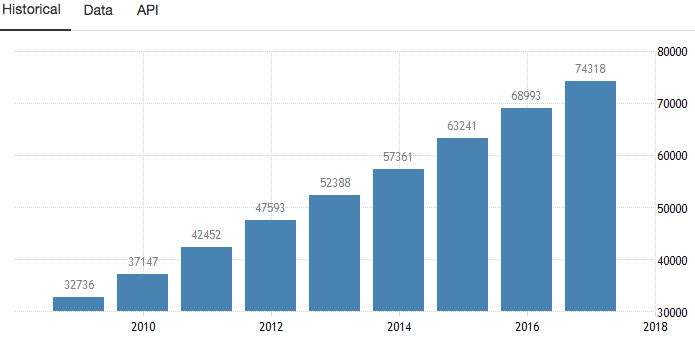

That might be correct, but I suspect the errors are actually much smaller. Here, it’s useful to start with some data that we can have more confidence in, average yearly nominal wage rates (divide by about 6.5 to get the dollar equivalent):

This matches all sorts of information from a variety of non-governmental sources. When I speak with people who live in China, I get the same impression of very fast rising nominal wages—both for professional jobs and low-skilled jobs like maids. When I read articles in the western media about wages in China, they tell the same story—very fast rising wages leading to many low-skilled firms moving to countries such as Vietnam.

It’s much harder to fake nominal wage data than GDP data because China’s a huge country and local citizens are quite willing to talk about their personal financial situation (unlike during the Maoist era when they would have been terrified to offer truthful information to reporters). To summarize, we can be almost certain that nominal Chinese wages have grown at explosive rates over the past decade, roughly 10 percent per year.

The second piece of evidence is China’s explosive growth in infrastructure, the sort of growth you’d normally see in a fast-growing economy like South Korea during the 1970-2010 period, not a Brazil or Mexico. Again, this is easily observed by visitors.

Explosive Growth

We also see explosive growth in various segments where western firms play a major role, such as auto production. This would be hard to fake. Ditto for China consuming a huge share of the world’s key commodities such as steel, coal, copper, cement, etc.

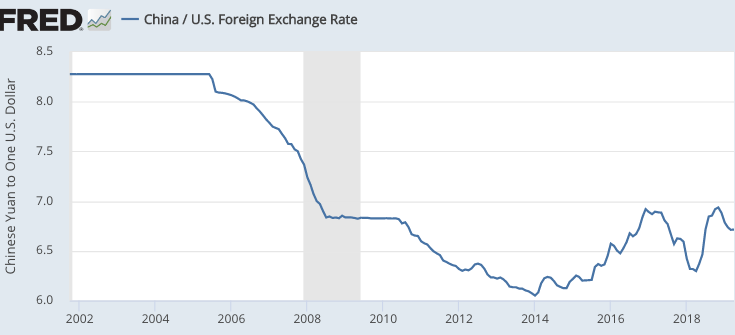

You might argue that the wage data is nominal and tells us nothing about real wages. That’s true, but we also have very good data on the dollar/yuan exchange rate, which has not changed much since 2009.

And note that the dollar itself is currently quite strong. If we combine the relatively reliable nominal wage data with the extremely reliable exchange rate data, we see that Chinese wages are also rising at very fast rates in US dollar terms. In addition, Chinese wages have grown much faster than wages in other East Asian countries, economies that are also growing fairly fast.

The developing countries in Southeast Asia have recently tended to grow at rates closer to 5%/year, which is roughly the rate that China would have been growing if their official GDP growth rate was overstated by 1.8%/year. But look at Chinese wages compared to those of other Asian economies. Does it seem plausible that China is growing at the same rate as Indonesia?

Is China’s Growth Understated or Overstated?

If China’s growth rate is consistently overstated, then China should be much poorer than what the official figures show. But if we compare China’s official GDP/person data to places such as Thailand and Malaysia, then the wage data makes it seem like China’s growth has been understated.

Then there is casual empiricism. If China’s growth were overstated, then visitors to China would be telling people, “Hmmm, this doesn’t seem like a country with a per capita GDP of $9600.” But if visitors do offer that opinion, it’s usually because China seems much richer than that figure. At one time, one could point to the fact that most Chinese lived in poor villages, but now most live in the cities. At one time one could argue that while the coastal cities were doing well, the interior remained poor. But now interior cities like Chongqing look quite affluent, as evidenced by this excellent NYT story.

I visited Chongqing in 1994, and recall a muddy, drab city full of crumbling grey cement buildings, with lots of poor people carrying heavy loads on their backs.

Again, it’s likely that the Chinese growth numbers are at least somewhat flawed. But when we look at all of the evidence, we cannot have confidence in the claim that Chinese growth has been greatly overstated. There is plenty of evidence in both directions.

PS: In my view, the Chinese boom has been caused by a huge shift of labor into the private sector, where the vast majority of workers are now employed.

PPS: People sometimes cite the fact that a Chinese leader once “admitted” that China’s growth was overstated. That’s not true. He admitted that the provincial growth rates are overstated, a point on which everyone agrees. The national statistical bureau scales back those local estimates before deriving a national growth rate. The issue at hand is whether their downward adjustment is large enough.

This article is republished with permission from The Library of Economics and Liberty.

Scott B. Sumner is the director of the Program on Monetary Policy at the Mercatus Center and a professor at Bentley University. He blogs at the Money Illusion and Econlog.

This article was originally published on FEE.org. Read the original article.

![]()