The latest issue of ‘The Globe’, Eurizon monthly publication describing the Company’s investment view. In this issue, a focus is dedicated to “The ups and down of inflation”.

Scenario

The overall scenario is characterised by moderating inflation, stable economic growth in the US, and signals that the slowdown is ending in the Eurozone. The central banks are keeping policy rates in restrictive territory but acknowledge that the debate on cuts has begun.

In January, inflation in the US came in higher than expected, albeit without compromising the downtrend. In the meantime, economic data confirm the solidity of the US economy and the gradual recovery of global trade, a positive development for the Eurozone, still highly dependent on exports.

The re-pricing of expectations referred to policy rate cuts continued. At the end of 2023, the markets were expecting the loosening cycle to start in March. Monetary market futures are now pricing in initial rate cuts, both by the ECB and the Fed, in June.

China is still injecting moderate economic stimulus, with the aim of achieving its 5% growth target, while preventing an overheating of the economy.

Geopolitical themes reaping modest impacts. US elections perceived as distant. The war in Ukraine and the tensions in the Middle East and Red Sea are no longer a surprise factor and are leaving macro variables unharmed.

Macro Economy

- The downtrend of inflation has slowed but is still converging towards central bank goals. Global economic growth is positive and proceeding at a moderate pace.

- Monetary market futures are pricing in stable Fed and ECB rates in the opening months of the year and will gradually lower then starting in the central months.

Asset Allocation

- The combination of stabilised inflation, positive growth, and declining policy rates, draws a favourable context for the financial markets.

- The bond markets are offering appealing coupon rates and spreads. Stocks are showing less appealing valuations than a year ago but may rise in line with earnings.

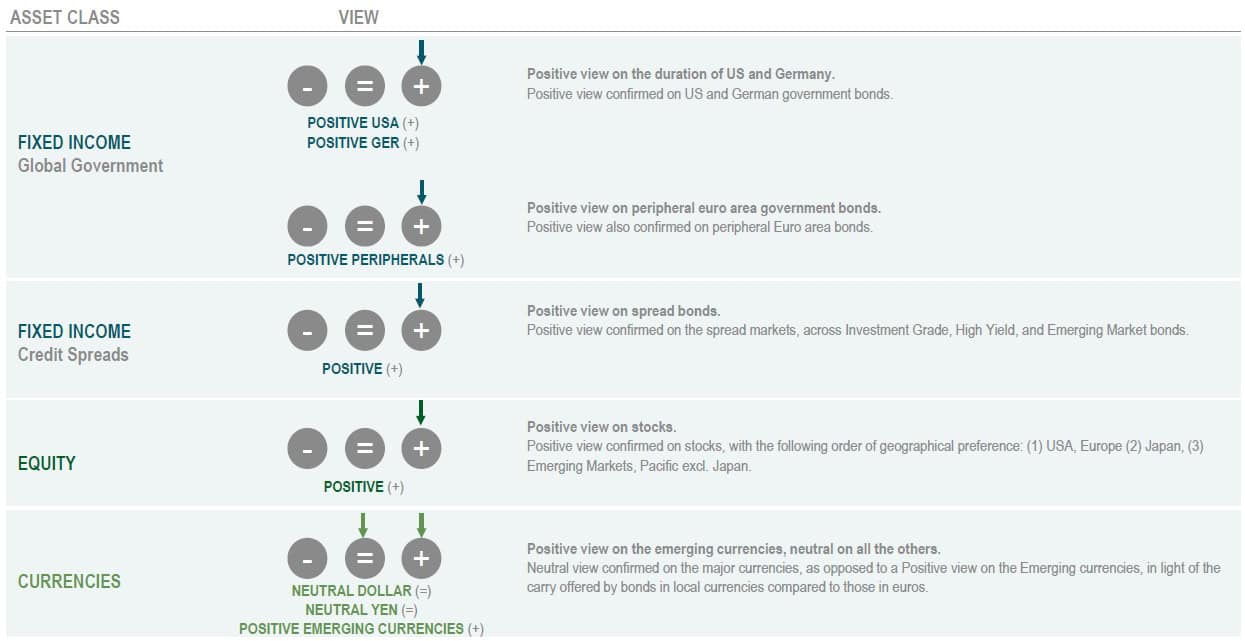

Fixed Income

- Overweighting confirmed of US and German government bonds, that offer appealing yield-to-maturity and are supported by expectations for interest rate cuts.

- The end of the monetary restriction is good news for spread bonds, that are showing historically appealing yield-to-maturity and spreads.

Equity

- The recovery in 2023 already partly prices in the positive evolution of the macro picture after the inflation shock, but corporate earnings may continue to grow, offering solid support to stock prices.

- By geographical region, our relative preference goes to the US and Europe.

Currencies

- The strength of the US economy, as opposed to the slowdown in Europe, could support the dollar, offset nonetheless by a less hawkish Fed in the present phase than the ECB.

Investment View

The baseline scenario combines inflation on the decline towards central bank targets with expectations for an ongoing global economic cycle. The ECB and the Fed intend to keep rates stable in the immediate term but have signalled they are open to cuts in the second half of the year. Geopolitical tensions are reaping a modest impact on the markets. Positive views on duration, the spread markets, and stocks.

Asset Classes compared

Yields rose in February, further balancing the partial correction recorded at the end of 2023. The US and German curves remain inverted. Spreads little changed for peripheral Euro area bonds, corporate bonds, and Emerging Markets bonds. The stock markets scored gains, with the S&P 500 and Eurostoxxindices marking new absolute highs. Dollar on the rise to 1.07 against the euro, yen still weak.

Theme Of The Month: The Ups And Down Of Inflation

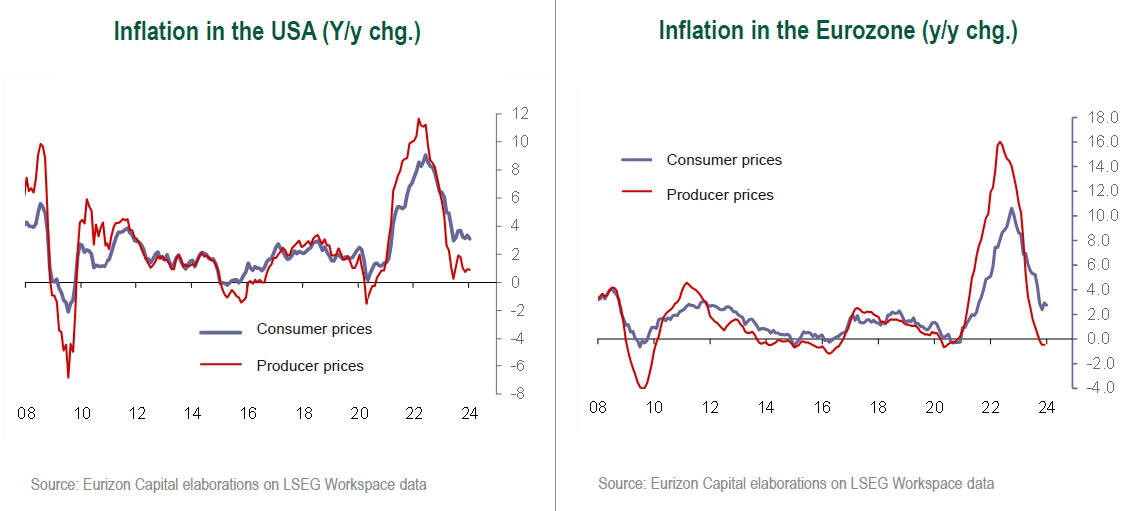

- The most prominent data release over the past few weeks was the US inflation reading for January, with both consumer prices and producer prices beating expectations.

- As the normalisation of inflation is the essential ingredient for a non-turbulent continuation of the economic cycle, these data deserve to be analysed.

- First of all, it should be said that data beat expectations on the upside, but not to the point of undermining the adjustment trend.In fact, in annual terms, consumer price inflation dropped between December and January from 3.4% to 3.1%, whereas producer price inflation is much lower, and in the past month has declined from 1.0% to 0.9%.

- Therefore, rather than a recovery of inflation, a stabilisation in the 1% area is taking shape for producer prices, and in the 3% area for consumer prices.

- In any case, in the current phase consumer price growth, from its present level of 3%, is converging towards the 2% target at a slower pace compared to the swift decline from recent highs (9% area in the US, 10% in the Eurozone).

- This is the “last mile” theme, the slowest phase of the process, and is the main reason for which the central banks are in no rush to declare that the fight against inflation is definitively over.

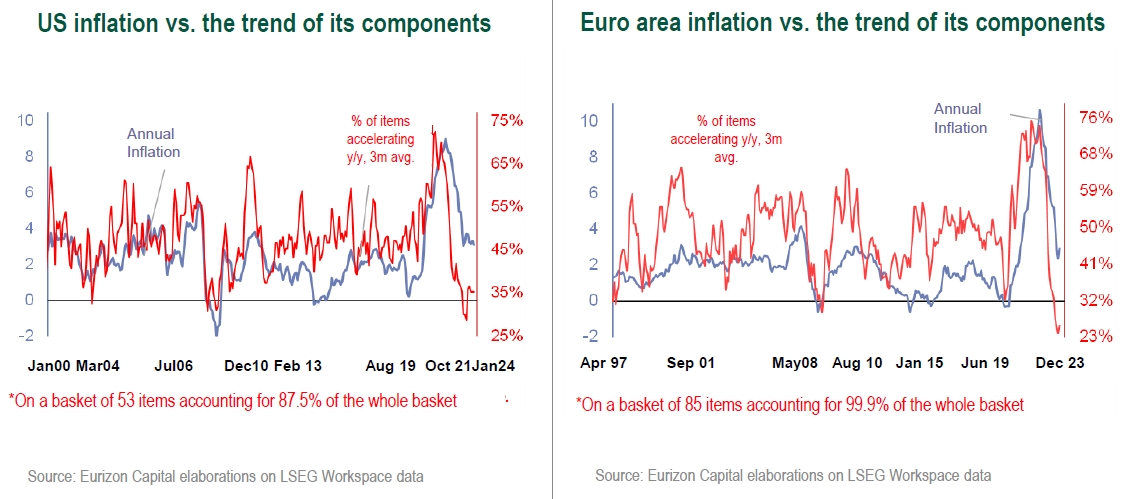

- The fact that inflation is undergoing a slowdown of its downtrend, rather than an upward inversion, becomes evident when analysingthe items that make up the consumer price basket.

- Both in the United States and in the Eurozone, the number of items that are showing a moderation of year-on-year inflation is much larger than those that are reporting an increase.

- These indicators, that at the peak of the inflation flare-up had punctually signalled the downturn, are not indicating an upward inversion at present, but rather a stabilisation.

- Furthermore, both in the US and in the Eurozone, there is a margin for the stabilisation to take shape at a lower level than the present, although there is no denying that the approach to the 2% target will be slow.

- The hypothesis of a stabilisation (rather than an upward inversion) is also confirmed by the markets. Inflation estimates drawn up by comparing the yield-to-maturity of nominal bonds and real rates have been pointing, for many months now, to stable breakeven inflation across maturities in the 2% area.

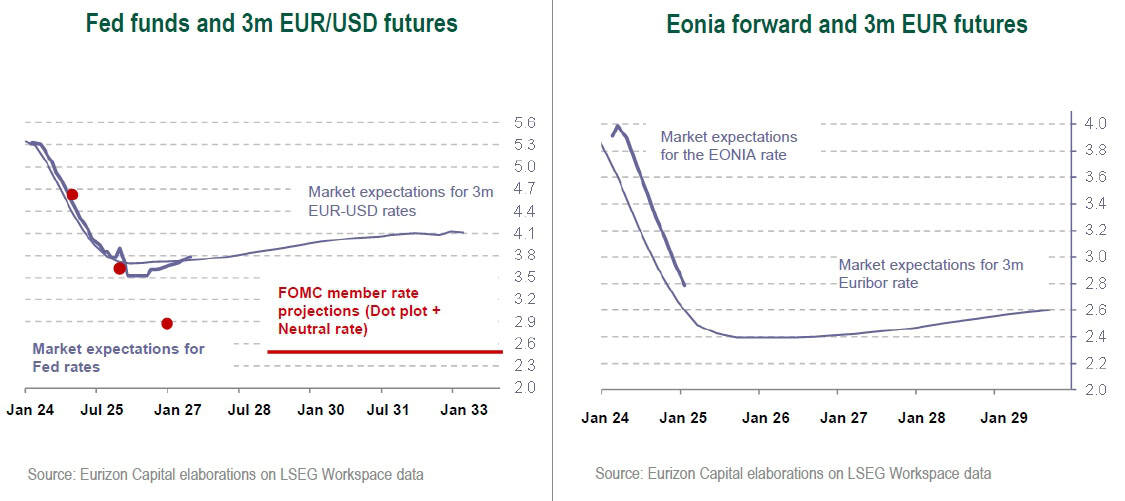

- The US inflation data helped continue the re-pricing of interest rate expectations, without overhauling them.

- At the end of 2023, the markets were expecting the accommodation cycle to start already in March. Now, monetary market futures are pricing in initial rate cuts, by both the ECB and the Fed, in June. Current expectations seem more realistic than those drawn up at the end of 2023.

- Going forward, based on the current forecasts implied by futures, the landing level of rates will be 3.0-3.5% for the Fed and 2.0-2.5% for the ECB. In both cases, 200 basis points below current levels, but well off the lows marked in the previous cycle.

- These expectations are also consistent with the end of the inflation shock, and with the continuation of the economic cycle: the ideal combination for the medium-term outlook.

- In the immediate term, the postponement of expectations may even continue, given the solidity of macro data, although the stabilisation of expectations should not be too distant in time. The ECB and Fed meetings, respectively on 7 and 20 March, will be important in giving investors some bearing in this sense.

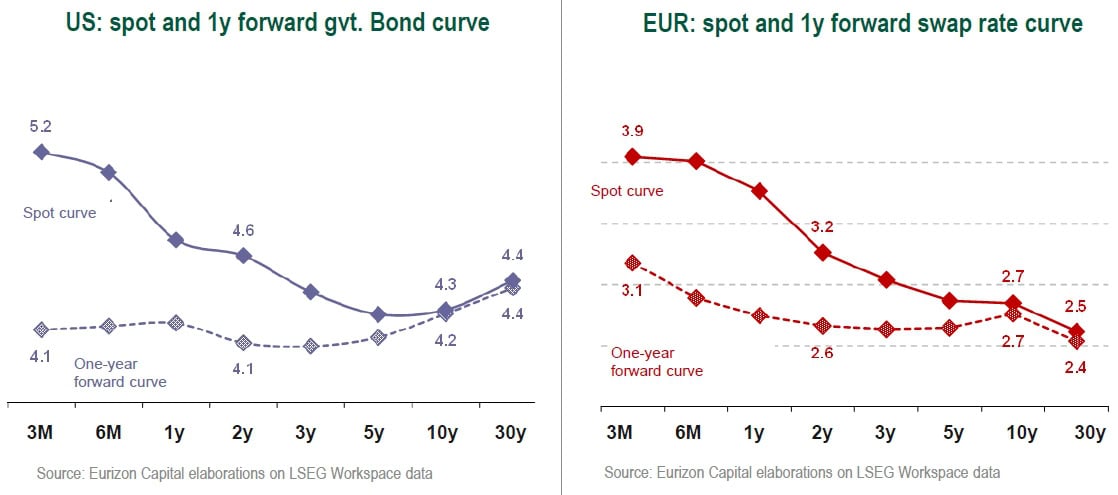

- The scenario that combines stabilising inflation and an ongoing economic cycle is also reflected by the slopes of government bond curves, that are inverted.

- Near-term rates, that are higher than long-term rates both in the US and in the Eurozone, imply the idea that central bank rates have now peaked, and that the next movement will be downwards. According to the forward curves, in one year’s time near-term rates will be one point lower than their current levels. At that point, maturity curves would be flat, but should take on a positive slope towards mid-2025, when the normalisation of central bank yields will have been completed.

- Based on the forward curves, longer-term government bond rates should move little from their present levels, despite the central banks’ policy rate cuts. This take implies expectations for the economic cycle to continue in the next few years. A reassuring hypothesis for the overall scenario and for the outlook for risk assets. However, this also indicates that the present level of long-term government bond yields represents a convenient insurance policy against the risk of a shorter than expected economic cycle.

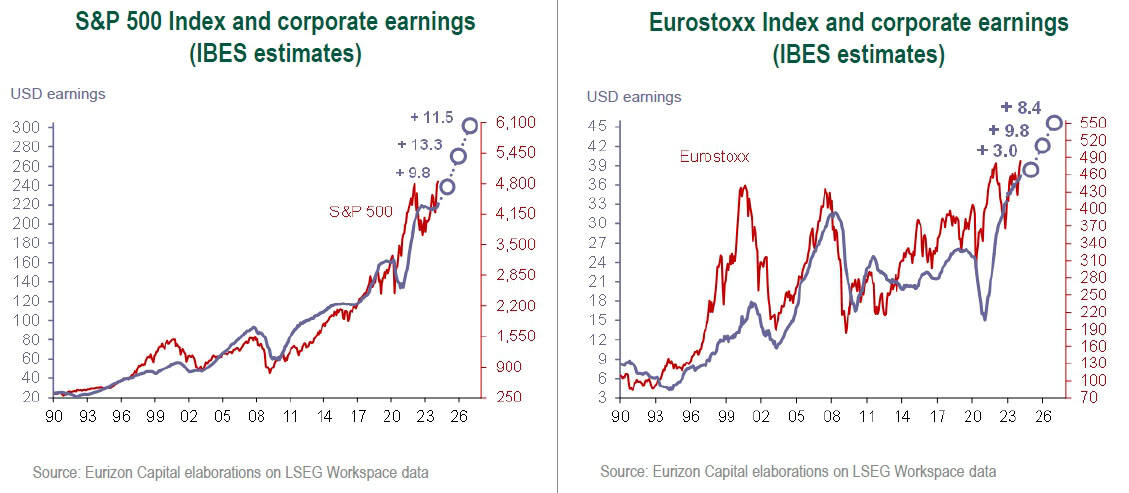

- The overall picture remains supportive for the stock markets, that in the past few weeks have marled new all-time highs, both in the United States (S&P 500 Index) and in the Eurozone (Eurostoxxindex).

- In the immediate term, the postponement of expectations for the start of the rate cut cycle may halt the upswing, also considering the speed of the upswing seen since November but does not seem to have the potential to significantly the underlying trend.

- The main source of support for stocks is earnings growth, recently confirmed by the 4Q 2023 reporting season.

- Analyst estimates point to an increase in corporate earnings this year, in 2025, and in 2026 as well, at a pace in line with the average for the previous cycles. These hypotheses seem realistic, assuming the economic cycle has finally found stability, after the turbulent post-Covid recovery phase, and may now proceed at its (moderate) cruising speed.