September marked the end of the third quarter and the Capital Ideas Fund returned +0.77% for the month and is now up +68.14% for the year. Many of our investment companies are executing very well, and their stock prices are reacting accordingly. We recently gave a keynote speech at the Planet Microcap Showcase in Vancouver. The presentation touched on our market outlook but the majority of it focused on breaking down past, present and future long-term compounding investments. These case studies are the focus of this newsletter. We place the most emphasis on the two future compounders, which are two of our largest investments in the fund.

We would like to highlight that we’re hosting an investor webinar on October 16th at 2pm. We will discuss our market outlook, interesting investment trends plus our top picks. We will save time at the end for questions. You can register HERE, or the information can be found on our LinkedIn page.

Jason will also be participating on the Keynote Panel at the Cantech Conference in Toronto on October 9th. Those interested can find more details HERE.

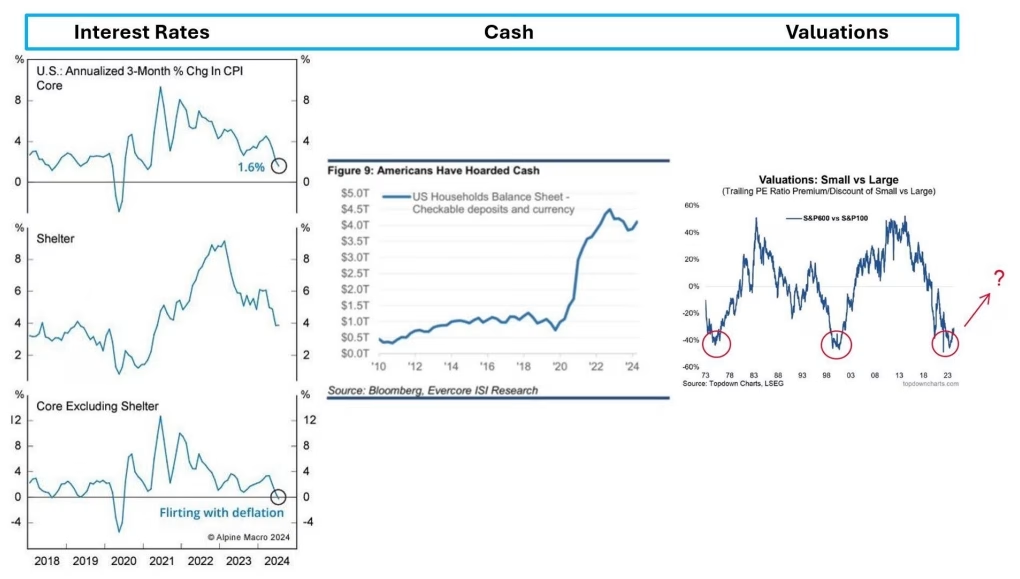

Rates, Cash, and Valuations

Since we published our last monthly update, the Fed cut interest rates by 50 bps. This tracks our market outlook where we’re now past peak inflation, and therefore peak interest rates. Rising interest rates during 2022-2023 was the major headwind to small- and mid-cap stocks and declining rates across the globe over the next few years should support a strong small- and mid-cap cycle.

As rates climbed higher and uncertainty hit a peak, the amount of cash that left the stock market and now sits on the sideline is at record highs, now approaching $7 trillion dollars. Past cycles have shown that as this money trickles back into the stock market it supports multi-year runs in stocks. We’re seeing empirical evidence of this as investors’ GICs mature, the rates at which they can re-invest are significantly lower and many are choosing to explore higher return avenues.

Even with a strong rebound in the fund since this time last year, we’re still seeing tremendous opportunities. Valuations are still depressed and we’re finding cheap stocks where the underlying companies are executing. Using current analyst estimates, small cap earnings growth is forecast to be 30% greater than large cap earnings growth in 2025. Add in the fact that small caps are at one of the historically cheapest discounts relative to large caps in history, and you’re getting a lot better growth and great prices. Combining these three points – declining rates, cash on the sidelines, and cheap valuations – supports our view that we’re at the beginning of the next multi-year cycle for small and mid-cap stocks.

Past Compounders

We want to highlight two past investments that we categorize as compounders. We think it is helpful to illustrate what we saw when we invested, how they performed over time, and why and when we exited. We’re using this as the first step in this exercise to establish what a compounder looks like and to help us identify the next big winners.

Before we jump in, there is a mental model which leads to a gap in the perceived value for these types of investments. Highlighting this issue will help understand the investment case for the stocks below. There is a gap in how compounding is perceived versus the real opportunity over time. Here is a quick example to illustrate.

If a stock trades at a 10x price to earnings ratio and grows earnings at 20% for 10 years and ends up at trading at 20x price to earnings, how much will that investment return?

Take a guess at what the return will be.

What we’ve found is most people will do some type of mental math like 20% x 10 = 200% plus double the multiple and get to 400% or something in that realm. The actual answer is +1,138% and it’s this gap in perceived value versus actual return where compounders are misunderstood and opportunity arises.

Now obviously, finding a company that can execute like this isn’t easy but not impossible. Let’s take a look at some examples below.

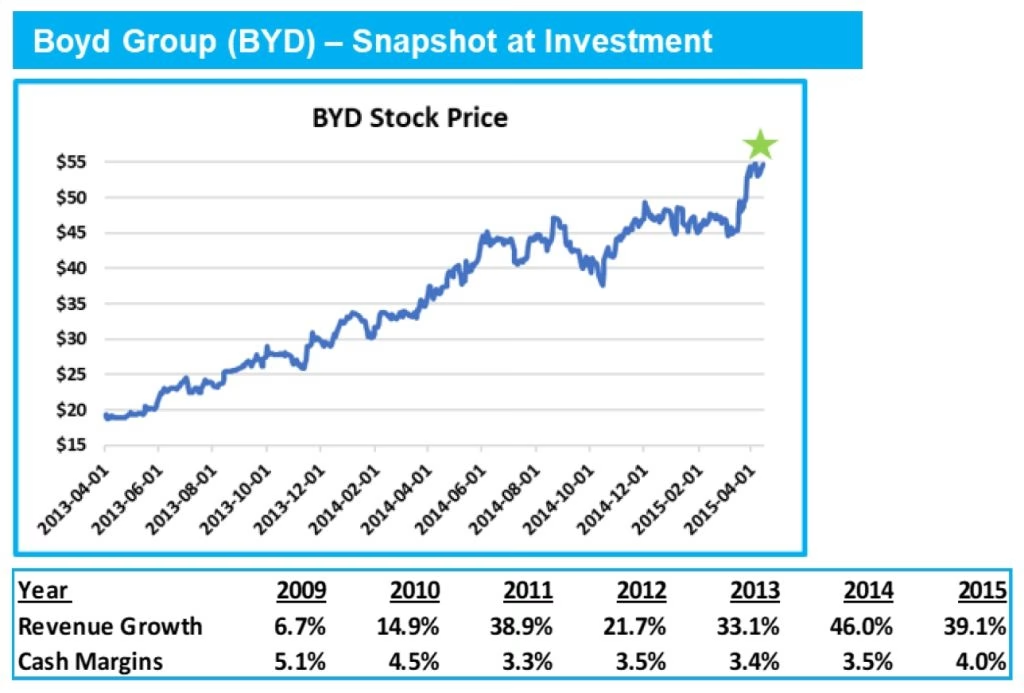

Boyd Group Services Inc (TSE:BYD)

Boyd Automotive owns auto repair shops across North America. We first invested in Boyd in April 2015 at $54.50/share (green star). Their historical revenue growth and cash earnings margin can be seen below. The IRR on each autobody was significant and they could take that internally generated cash and use it to open more locations across North America. The top line growth was already evident, and the stock price was already strong but that didn’t mean the story was over.

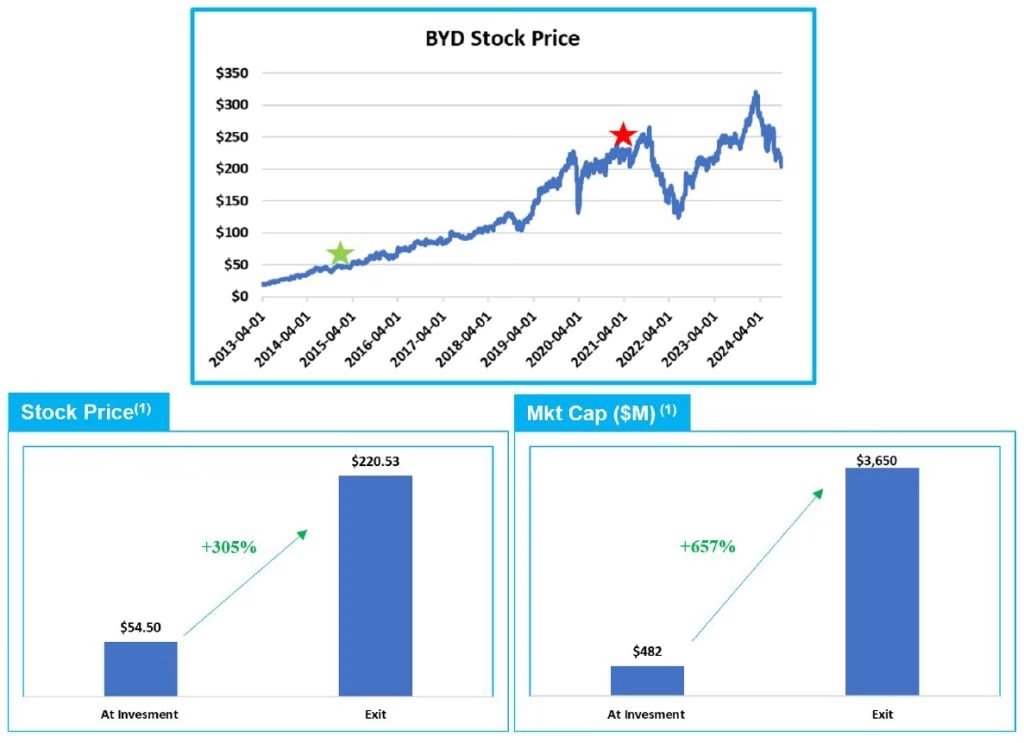

Over the next 7 years the stock would go from $50 to over $250. We exited the investment at ~$220 as the rate of compounding began to slow and their valuation wasn’t cheap plus we could find better investment opportunities.

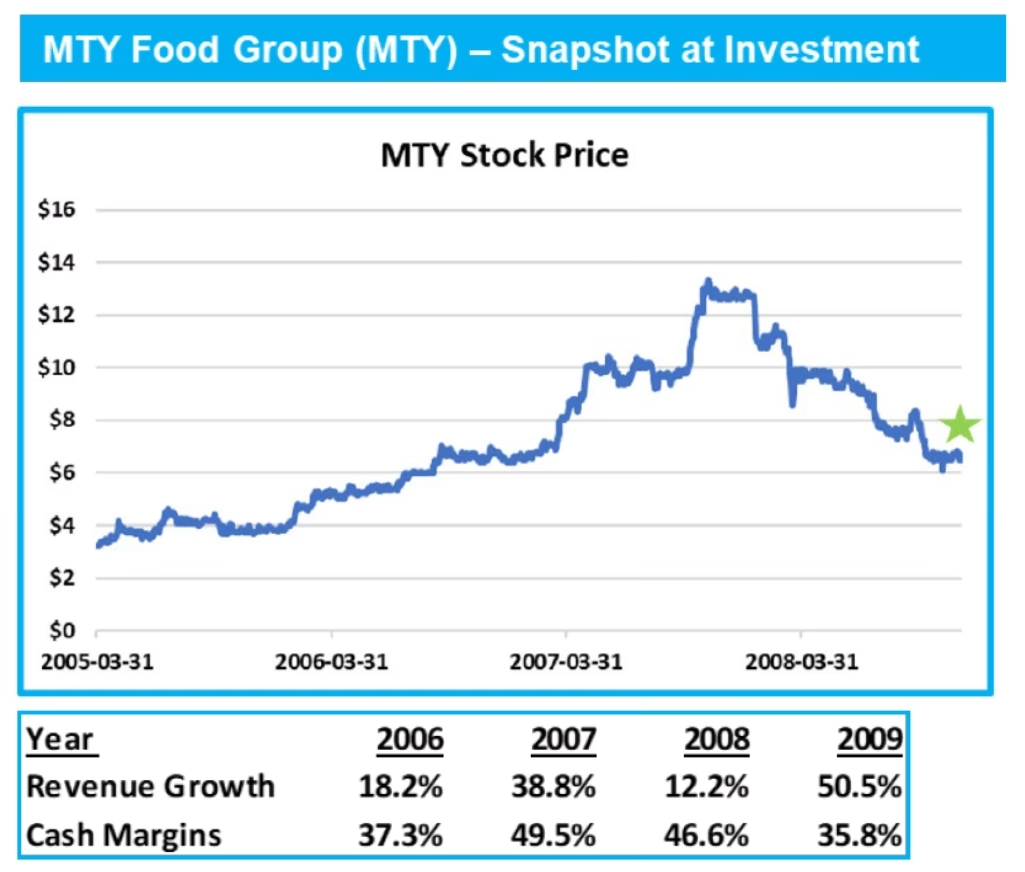

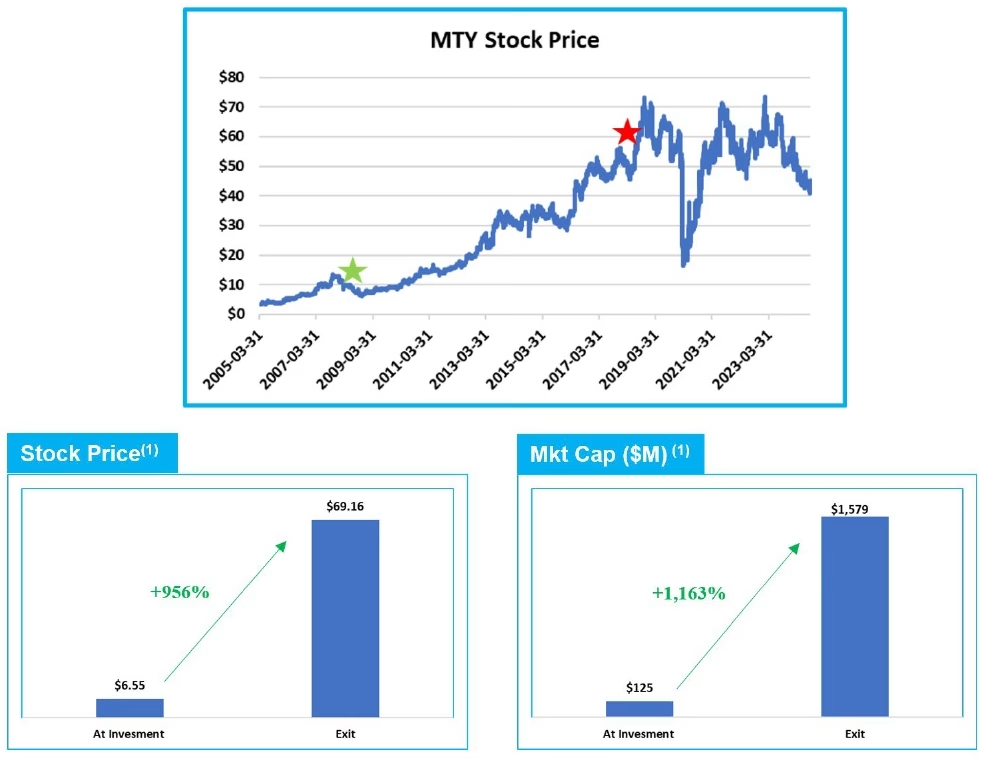

MTY Food Group Inc (TSE:MTY)

We first invested in MTY in December 2008 at $6.55/share. Their CEO, Stanley Ma, was acquiring food court brands and improving their profitability and taking that cash flow to invest in more food court brands. This strategy had a high ROI and a long runway for growth as he expanded across Canada.

We sold the position around $69/share in 2018 as our calculation of ROE started to decline. The business had successfully grown across Canada and the ROI on new investments didn’t appear to be as great.

Current Compounders

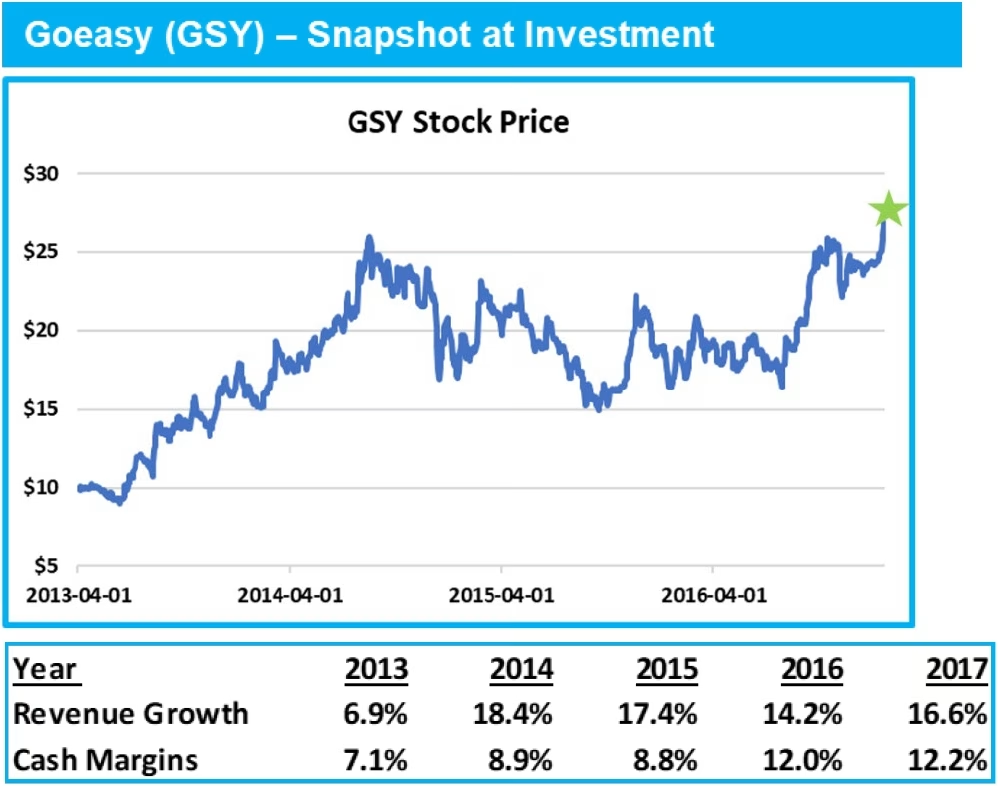

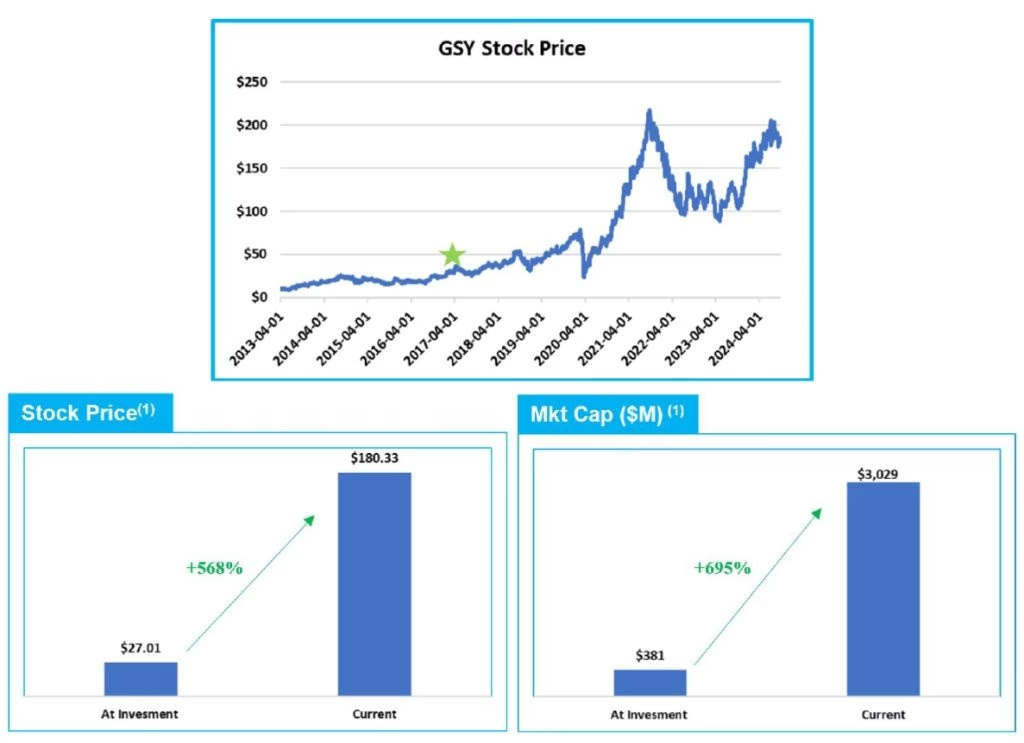

goeasy Ltd (TSE:GSY)

We first invested in GoEasy in January 2017 at $27.01/share. As you can see from the historical financials, they were consistently growing and margins were expanding. GoEasy could lend a $1 and make +$0.20 profit per year on it, leading to +20% ROE year over year.

GoEasy is still generating an ROE well in excess of 20% and we still see a long runway for growth as they expand product offerings and take more market share.

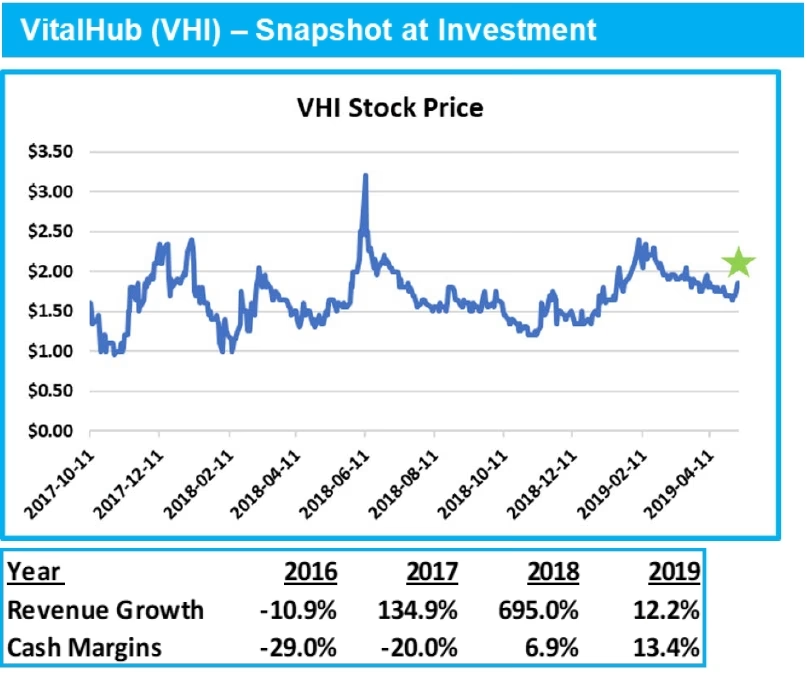

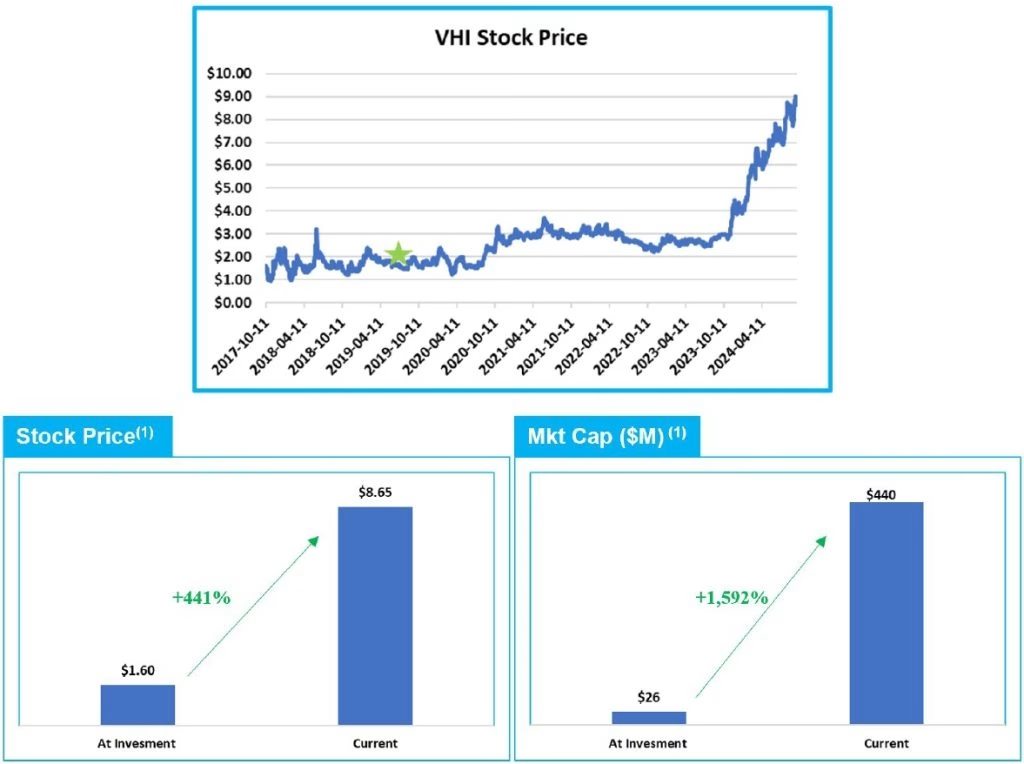

Vitalhub Corp (TSE:VHI)

We first invested in VitalHub in May 2019 at $1.60/share. In 2017 & 2018 the management team acquired the first couple of assets that laid the groundwork for what VitalHub would evolve into. They had prior experience and success in the space and knew how to acquire (allocate capital) well and scale a business. We invested once we could see cash margins start to pick-up.

Since 2019 VHI management has executed well and have balanced acquiring assets, growing organically, and improving margins. The stock really jumped late last year when they reported strong profitability and cashflow, and we think that’s when the market started to realize how profitable this company really is. Today, they are sitting on a large amount of cash, which we expect to be deployed by year-end which will just be a continuation of compounding capital at high rates of return. Their ability to acquire low or no margin businesses with complimentary technology and then integrate and cross-sell plus significantly improve margins has been a winning formula and also a repeatable formula. We expect VitalHub to continue to execute and eventually be put in the category of other great compounders using a similar strategy, like Constellation, Enghouse & Descartes.

Future Compounders

To be a long-term compounder a company needs:

- Profitability

- Ability to re-invest at high rates of return

- Long runway for compounding

In the examples above, each company is highly profitable and generates significant operating cashflow. In each case – autobody shops, food court restaurants, subprime lending, and healthcare software companies – they were able to take that profit and re-invest into buying or building more of the same high ROI assets. Boyd went from 1 location in 1990 to over 800 locations today. MTY went from 1 location in 1979 to over 7,000 locations today. GoEasy opened its first easyfinancial branch in 2011 and now has over 300 branches across Canada. VitalHub started with 5 solutions in 2017 and now has close to 60 products and solutions.

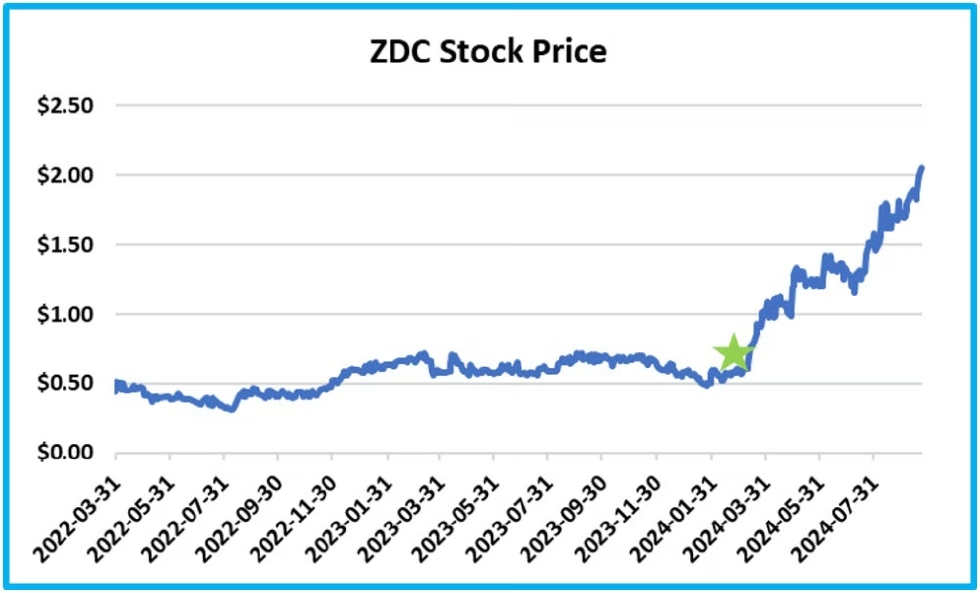

Zedcor Inc (CVE:ZDC)

We have written about Zedcor now a few times from a couple of different angles. See HERE & HERE. Today we’re addressing how Zedcor is showing the signs of being an early long-term compounder.

To start, Zedcor is already very profitable. Last quarter they reported 40% cash earnings growth with 20% cash earnings margins. Second, we calculate that their IRR for their security towers is +40%. This is obviously a very high IRR which is now generating a significant amount of operating cashflow. They are taking all of this cashflow and recycling back into the business to build more towers which will generate +40% IRRs and so the compounding train begins to roll. Third, the end market seems to be much larger and unpenetrated than many might assume. Zedcor is currently just over 1,000 towers and guiding to being double the size by this time next year. We see the roadmap and demand for them to be at 10,000 towers within a few years. That is 10x the size they are now and that will still only represent a few percent of the addressable market. We expect them to report over 80% revenue growth next year with over 100% earnings growth but the story is now taking shape for this to be a long term compounder like the ones discussed above. They are currently across 6 major cities in Canada and Houston, Texas in the US. If they continue to execute, there could be tens of thousands of towers across North America.

Enterprise Group Inc (TSE:E)

This is the first time we’re writing about Enterprise Group. The stock is performing well and has grown into a large position within the fund. The company has been around for a long time but what attracted us to the company has only emerged within the last couple of years. The business offers all the oilfield service equipment one might expect, but it is their Evolution Power Projects (EPP) division that is driving over 40% growth in cash earnings this year. EPP offers mobile power supply for energy companies that saves the client 80-90% in costs, is more reliable, and reduces emissions significantly. Their product is a great ROI for the client which allows Enterprise to generate significant margins and ROI for themselves. We estimate this division generates +50% IRRs and the fact that they have an exclusivity agreement for the underlying technology, gives them the runway to go from 30 units to hundreds within energy the sector, and hundreds more within the mining sector.

*A note to make on both ZDC & Enterprise is that we believe we’re in the first innings of their growth story. Their stock prices have obviously performed well recently, but much like when we invested in Boyd Group or GoEasy early on, the stock charts may have looked like “we already missed it” which we view as a flawed investment mentality, at least when it comes to long term compounders.

Other Company Notes

Propel Holdings Inc (TSE:PRL)

Announced the acquisition of Quidmarket on September 26th, for $71m USD. They raised $115m CAD at $27.50 to fund the deal all in cash. It is immediately accretive to earnings based on the multiple paid and the high profit margins at Quidmarket. This now gives Propel a third geographic avenue for growth.

Final Thoughts

As interest rates continue to rollover, sitting in cash becomes a lot less attractive and stocks more so. The massive gap in large-cap versus small-cap valuations should narrow. This should lead to the next multi-year cycle for small cap stocks. We aim to invest in stocks like the ones discussed above and believe the future is bright for compounding stocks.

Please reach out directly if you have any questions about our investing strategy, any of the points supporting our economic views, or specific companies.

Sincerely,

Jason & Jesse