Crescat Capital Crescat Capital commentary for the month of December, 2023, titled, “deconstructing the powell pivot.”

Season’s Greetings and Happy Holidays from Crescat!

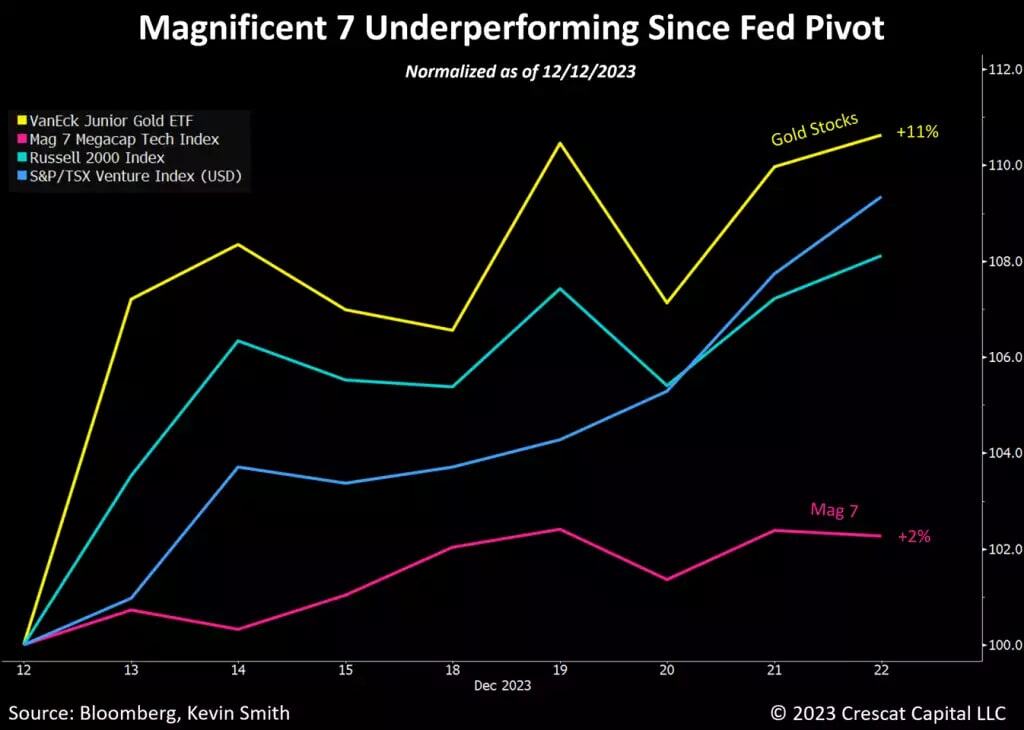

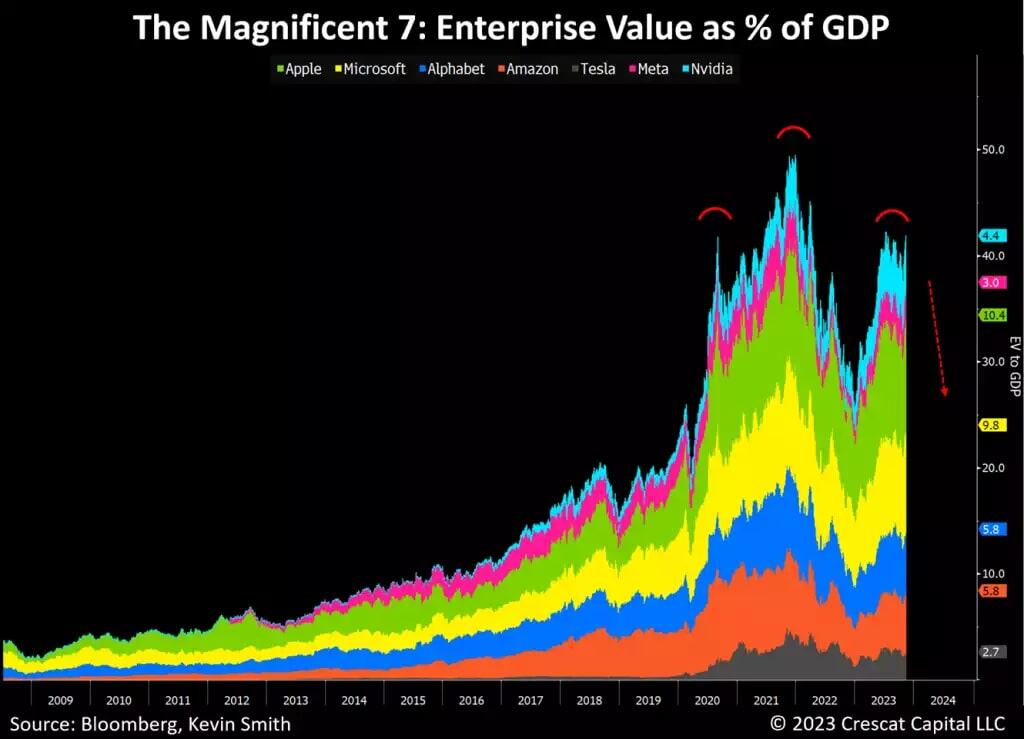

Our overriding Great Rotation theme just received a jumpstart with the Fed’s pivot to easier monetary policy at its December 13 meeting. Jerome Powell and Company signaled lower interest rates in 2024. Since the central bank’s shift, note the outperformance of undervalued junior gold mining stocks, including the exploration-heavy TSX Venture Exchange Index, and small cap stocks in general compared to the crowded and overvalued megacap tech behemoths. We illustrate this strong relative performance in the chart below.

Q3 2023 hedge fund letters, conferences and more

This unfolding divergence favors the deeply depressed small and microcap metals explorers which are ripe for outperformance as we have been saying in our recent letters. We have remained positioned for this major theme across the firm. As a result, each of our strategies is up significantly month-to-date. We believe there is much more to play out, hopefully in the final week of 2023, but especially in the months, quarters, and years ahead.

- Inflation to be the Ultimate Deflator of Financial Asset Bubbles

- Beware the Soft-Landing Narrative: Stagflationary Recession More Likely Ahead

- Suppressed Commodities Have Room to Run

- Crescat Precious Metals Fund

- Crescat Global Macro and Long/Short

- Nasdaq 100 Double Top

- Performance of Crescat Strategies Since Inception

Inflation to be the Ultimate Deflator of Financial Asset Bubbles

It is important to note that the Fed’s interest rate hiking campaign, which has now come to an end, achieved nothing significant at all, in our analysis, in alleviating the four major fundamental long-term structural inflationary headwinds that we have highlighted in our prior letters. This is what we have referred to in the past as the four pillars of inflation: (1) deglobalization, (2) resource underinvestment, (3) wage-price spirals, and (4) the ongoing central bank monetization of extreme fiscal debt and deficits.

The Fed helped create many of these embedded inflation problems in the first place due to too many years of ultra-accommodative monetary policy which served primarily to create only bigger and bigger debt and financial asset bubbles. Now, we believe the Fed has little choice but to tolerate long-term rising consumer and wholesale prices as it attempts to manage the deflation of these bubbles.

The Fed’s toolkit for fighting inflation is limited primarily to short-term (i.e. transitory) demand destruction measures through its aggressive interest rate increases. Historically, such a policy has always triggered a recession, often with a lag, and ultimately coinciding with the bursting of asset bubbles. We expect this time will be no different.

Beware the Soft-Landing Narrative: Stagflationary Recession More Likely Ahead

Despite abundant recession signals, the highly popular narrative remains that Powell is likely to “stick the soft landing”. Generous soft-landing narratives are historically common immediately ahead of economic contractions. The facts are that soft landings are extremely rare and historically nonexistent in the wake of aggressive rate hikes like those already implemented from March 2022 to July 2023. At Crescat, we remain highly committed to our significant long precious metals exposure as our primary means of navigating the likely pending stagflationary recession.

In our analysis, Powell’s pivot was driven by the abundance of indicators signaling the high probability of an approaching hard landing. We enumerated these warning signs in our November 26 letter. Because the central bank made this policy reversal before achieving its inflation target, it was confirmation for us that it was capitulating to the high risk of recession, especially given the losses and potential further losses in the banking and financial system created by higher rates. It was not giving in because it had conquered inflation.

The risks of a banking and financial system crisis were evident as of late October when 10-year yields hit a recent peak just above 5%. At that point, the banking system had just incurred an incremental $125.5 billion unrealized loss on its securities held and a $90.4 trillion decline in bank deposits in its third quarter. This was the same problem that created the bank failures in the first quarter. In our opinion, the Fed pivoted to help the banking sector, especially after giving recognition to likely broader credit losses in the system that have yet to be officially recognized.

Indeed, credit markets have had an enormous relief rally since 10-year US Treasury yields peaked just north of 5% on October 23 and are now down to 3.9%. Meanwhile, 2-year yields have dropped from 5.3% down to 4.3%. It is important to point out that plunging yields as such are normally associated with Fed easing ahead of and during recessions. We think this time will prove no different. The 10-year vs. 2-year yield spread is still inverted. It has been inverted for 18 months now, which is toward the long end of its historical range for this indicator whereby inversions have historically signaled an impending recession. Yield curves normally un-invert only as the recession unfolds. We expect the economic contraction to kick off in the first half of 2024 coincident with a significant decline in crowded megacap tech stock fundamentals and stock prices.

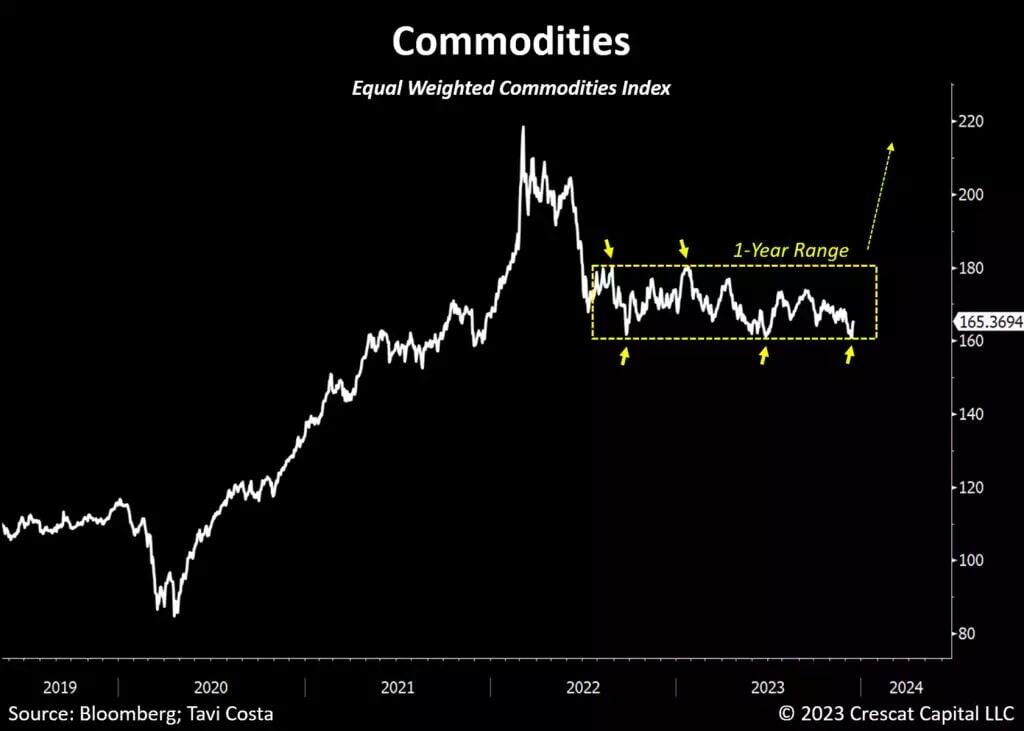

Suppressed Commodities Have Room to Run

During the likely coming decline in the real economy, we expect to see the re-emergence of commodity price inflation due to high fiscal deficit spending and cumulative years of critical resource underinvestment combined with a more accommodative Fed making this a stagflationary style of hard landing similar to 1973-74 where commodities and commodity stocks performed spectacularly. The early 2000s was another macro analog where it behooved hedge funds and nimble investors to be long commodity-oriented stocks and short large cap tech stocks, even during the onset of the recession and especially during the bursting of the tech bubble. The technical setup today for commodities is particularly strong after the recent sideways trend for more than a year in the equal-weighted commodities index.

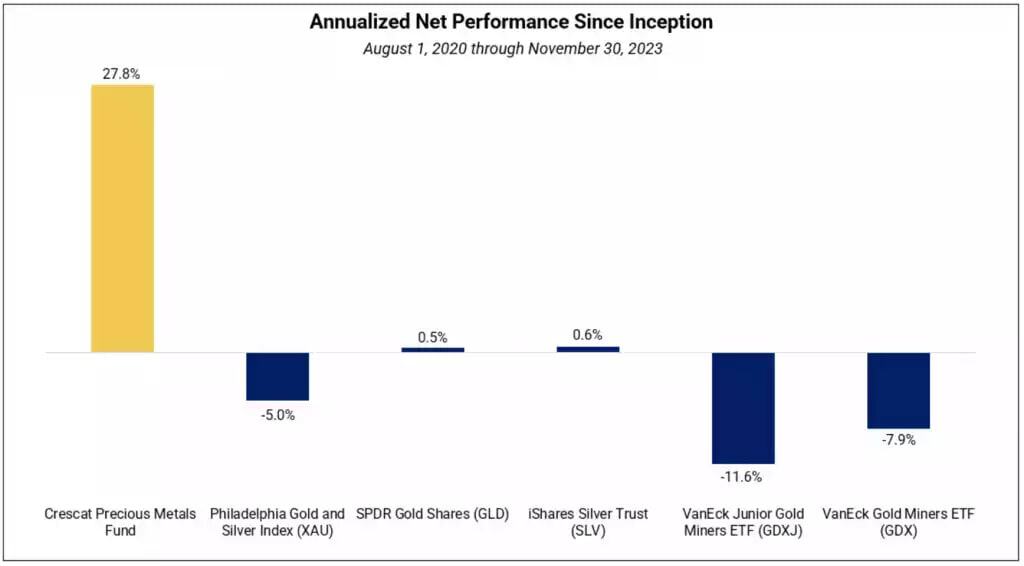

Crescat Precious Metals Fund

We encourage qualified investors to consider our Precious Metals Fund which has substantially outperformed its peers and benchmarks in the more than three years since its inception. We accomplished this ultra-high alpha in a bear market for precious metals mining stocks staying fully invested in them on the long side the entire time in accordance with our activist exploration strategy. The bulk of the credit goes to our Geologic and Technical Director, Quinton T. Hennigh, PhD for his ability to identify and help create major early-stage discoveries. What we remain most excited about is to show what we believe we can do in the likely coming precious metals bull market.

Performance data represents past performance, and past performance does not guarantee future results. Performance data is subject to revision following each monthly reconciliation and/or annual audit. Historical net returns reflect the performance of an investor who invested from inception and is eligible to participate in new issues. Net returns reflect the reinvestment of dividends and earnings and the deduction of all fees and expenses (including a management fee and incentive allocation, where applicable). Individual performance may be lower or higher than the performance data presented. The performance of Crescat’s private funds may not be directly comparable to the performance of other private or registered funds. The currency used to express performance is U.S. dollars. Investors may obtain the most current performance data and private offering memorandum for Crescat’s private funds by emailing a request to info@crescat.net.

Crescat Global Macro and Long/Short

For those looking for an even more comprehensive way of attempting to capitalize on the unfolding macro environment, we encourage you to consider our Global Macro and Long/Short funds. There we remain committed to our short positions in megacap tech stocks today in addition to our activist long precious metals and other commodity long exposures combined with a variety of other macro themes.

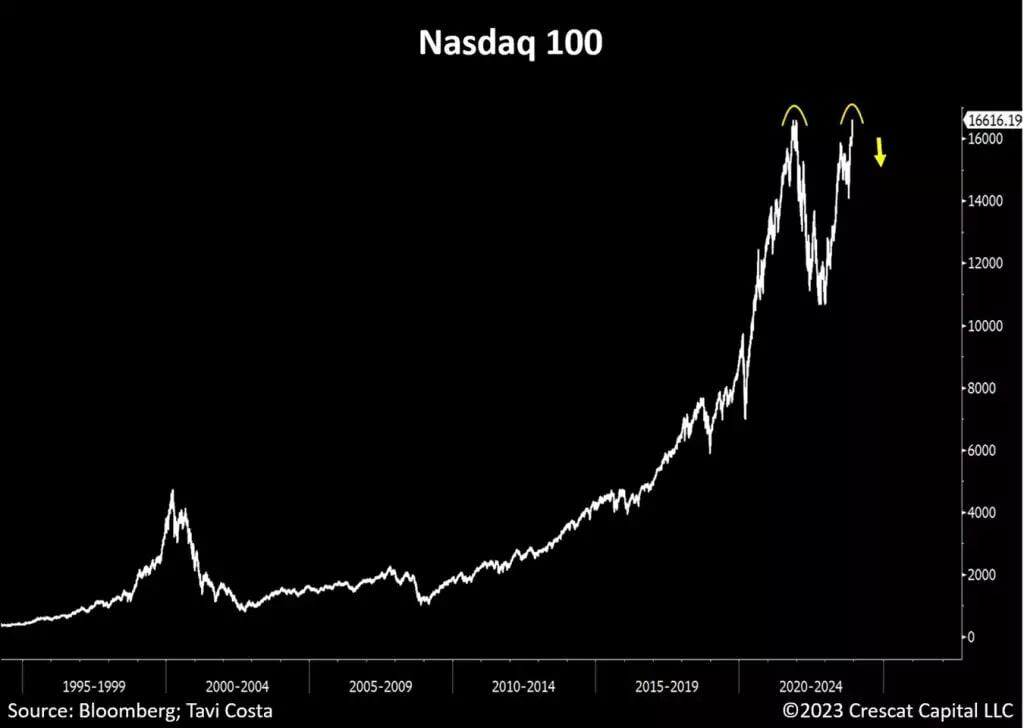

Nasdaq 100 Double Top

Our mega-cap tech short positions worked for us in 2022 when they first peaked but held us back in 2023 during what we believe is a bearish double-top retest now poised to fail. Imagine it is late 2021, and you have the chance to short mega-cap tech all over again from the top, this time just ahead of a likely recession. Our Global Macro and Long/Short investors have this opportunity now.

Performance of Crescat Strategies Since Inception

We believe our Great Rotation theme is getting ready to play out in full force. We are confident there is much more still to capitalize on in favor of our dedicated long-term clients for whom we are extremely grateful. As we are about to enter a contentious presidential election year, we sometimes hear the idea that election years are historically good for the S&P 500. That had been the case on average only a few decades ago. But then came 2000 and 2008, so we would be careful with such assumptions.

Performance data represents past performance, and past performance does not guarantee future results. Performance data is subject to revision following each monthly reconciliation and/or annual audit. Historical net returns reflect the performance of an investor who invested from inception and is eligible to participate in new issues. Net returns reflect the reinvestment of dividends and earnings and the deduction of all fees and expenses (including a management fee and incentive allocation, where applicable). Individual performance may be lower or higher than the performance data presented. The performance of Crescat’s private funds may not be directly comparable to the performance of other private or registered funds. The currency used to express performance is U.S. dollars. Investors may obtain the most current performance data and private offering memorandum for Crescat’s private funds by emailing a request to info@crescat.net.

We encourage you to reach out to any of us listed below if you would like to learn more about how our vehicles might fit with your individual needs and objectives.

Sincerely,

Kevin C. Smith, CFA

Founding Member & Chief Investment Officer

Tavi Costa

Member & Macro Strategist

Quinton T. Hennigh, PhD

Member & Geologic and Technical Director

For more information including how to invest, please contact:

Marek Iwahashi

Investor Relations Coordinator

Linda Carleu Smith, CPA

Co-Founding Member & Chief Operating Officer

© 2023 Crescat Capital LLC