Absolute Return Partners’ letter for the month of September 2024, titled, "Why it is a bad idea to raise tariffs."

"We will impose stiff penalties on China and all other nations as they abuse us." - Donald Trump

Higher tariffs? Really?

International trade has always been a source of great wealth. Take a look at some of the finest cities in the world – they are all packed with outstanding culture and great wealth. How do you think Amsterdam became one of the wealthiest cities globally? Not to mention London or New York City. It is hard to find a single A-list city anywhere in the world that didn’t build its wealth on international trade.

My first reaction, therefore, when I heard that Donald Trump intends to limit international trade by raising import tariffs was sheer horror. OMG, I said to myself. Does he understand what he is doing? And my anxiety level rose to new heights when I realised that Kamala Harris is planning to do the same. If you don’t believe me, I suggest you read this.

Trump’s and Harris’ stance on tariffs is not about economics, though, but about politics. They both know that a large proportion of the US workforce is in favour of restricting non-US companies’ access to the US market. Election day is coming up, and every vote counts.

The proposal

Little has yet been published on Harris’ plans, so let’s focus on Trump. He has proposed that, when he returns to the White House next January (his words, not mine), he will definitely raise tariffs on imported goods. When you want to assess the possible damage, it gets a bit complicated, though, as he has presented about five different models so far.

One of those models suggests a 10% tariff on top of existing import tariffs on all imported goods and services ex. those from China. China will be treated as a special case. Today, goods and services imported from China are due 12% in import tariffs. Trump introduced that number during his 2017-20 tenure, and Biden hasn’t touched it. More recently, Trump has indicated that he plans to raise import tariffs on goods and services imported from China to 60% (!).

Such a strategy is poorly thought out, and the reason is that tariffs are far less effective than they were, say, 100 years ago. In simple terms, tariffs no longer address trade imbalances because most trades do not settle bilaterally anymore. That may have been the case 100 years ago, when transportation costs were too high to allow production across many locations,but it has become less true over time.

Therefore, higher tariffs will most likely be an economic failure, but that doesn’t prevent such a programme from becoming a political success. What do I mean by that? Economics first. Despite thousands of manufacturing jobs seemingly being created by Trump last time, in a study from December 2019, economists from Federal Reserve found a net decrease in manufacturing employment caused by the higher tariffs.

As far as the political angle is concerned, David Dorn of the University of Zurich has phrased it very succinctly: “People react very positively, positively from a Republican point of view, to import protection of their local industry, [and] they don’t punish Republicans that much if their location gets exposed to retaliatory tariffs.” (source: New York Times).

Dorn refers specifically to Trump’s tariff plans, but you can replace R with D at your own will. To both camps, tariffs appear to be a key policy point in the current election campaign. It is important to understand that, although tariffs fail all economic tests, they are politically motivated and, for a presidential candidate, it is not about economics but about securing votes.

How likely is it to happen?

The 10/60 model is only one of a handful of proposals that Trump and his advisers are floating around. The water is clearly being tested. It is still too early to say which model we’ll end up with, but it seems certain that tariffs will increase under the next President, whether we end up with him or her. The only questions are (i) which countries will be targeted and (ii) by how much?

The 10/60 model is clearly the most dramatic proposal that has been shared with the public so far. A less dramatic model is based on a range of tariffs – from 5% to 60% depending on the type of good or service in question – and that model points towards a 19 percentage points increase in tariffs on goods and services imported from China. The jury is still out whether that model will increase tariffs on imports from other countries than China.

The problem the Americans are up against is that higher tariffs almost always lead to retaliation, which is effectively why the claim that higher import tariffs will lead to more jobs at home is incorrect. Retaliation is akin to trade war, i.e., the more the American raise US import tariffs, the more likely it is that we end up in a nasty trade war which is bad for everybody, as it is bad for both GDP growth, inflation and equity returns worldwide.

And that is precisely why none of the candidates, in my opinion, are likely to go for the model that will cause max. damage. Such a model will be ill received on Wall Street, and both candidates will need plenty of support from there to win in November.

What happened last time and what is likely to happen this time?

The United States is a net importer of goods and services to the tune of about $1 trillion annually. The 2017-2020 Trump Administration increased tariffs by roughly $80 billion during its tenure, and the CBO has estimated that the programme cost each US household about $1,300 in 2020.

A 10% tariff on all imported goods and services would have a similar effect, with middle-income families facing at least $1,700 in additional annual costs, potentially up to $2,400 if tariffs are fully passed on to consumers. If a 60% tariff were levied against China, middle-income families would face almost $4,000 of additional costs annually.

Estimating the impact on US households is in fact rather tricky. You do not know to what extent consumers change their shopping habits. Do they take the price increase on the chin, or do they substitute the goods and services in question with goods and services from countries which are subject to lower tariffs?

The estimated net effect

Tariffs rarely work out as planned, and there are (at least) three reasons for that:

- when you introduce (higher) tariffs, there is no guarantee that you reduce the amount of imported goods and services. You might just increase price inflation instead. The consensus is that a 10% US tariff on all imported goods and services will raise US CPI by about 1% in the first year after implementation, quite possibly leading to a more hostile Fed;

- when you raise import tariffs on, say, Chinese goods, consumers may choose to buy the same goods from other countries (e.g. Vietnam), i.e., the overall trade balance may not be affected to a meaningful degree; and

- the types of jobs that the US has lost to import competition from, say, China in the past are quite different from the types of jobs that would be created if those same industries were to expand operations today, meaning that the potential employment gains from new tariffs will most likely be much smaller than the employment losses from earlier import competition.

… and, for those reasons, it is difficult to predict which model the two candidates will go for, and precisely what the impact will be. That said, we know for a fact that US inflation will rise, and we know that US GDP growth will decline.

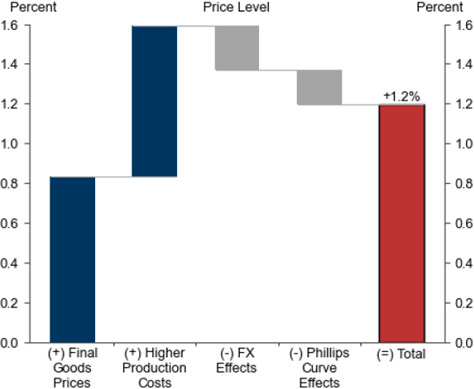

If we assume that we will end up with 10% across-the-board import tariffs on all countries ex. China and on the scaled model introduced earlier on imports from China, a detailed analysis conducted by Goldman Sachs Research suggests the following will happen: US inflation will increase by 1.2% in the first year after implementation (Exhibit 1) whereas US GDP growth will be 0.6% lower than it would otherwise have been (chart not included).

Exhibit 1: Effect on US inflation from a 10% gen’l tariff, 20% on China

Source: Goldman Sachs Global Investment Research

The result doesn’t really surprise me. Tariffs are bad – full stop - but the fact that the penny has not yet dropped on the two candidates is probably the most surprising part of this analysis. Then again, to them, it is about getting elected, not about economics.

Niels

2 September 2024

Investment Megatrends

Our investment philosophy, and everything we do at ARP, is driven by the long-term Investment Megatrends which are identified and routinely debated by our investment team.

About the Author

Niels Clemen Jensen founded Absolute Return Partners in 2002 and is Chief Investment Officer. He has over 30 years of investment banking and investment management experience and is author of The Absolute Return Letter.

In 2018, Harriman House published The End of Indexing, Niels' first book.