Seth Fischer walked on stage at the 2026 Sohn Montreal Investment Conference, looked at the room, and asked who had been to Japan. Plenty of hands went up. “Okay, great, I think I’m done then,” he said. He was not done. The founder and chief investment officer of Oasis Management has spent 31 years investing in Japan, and he used his slot to argue that the country is finally a place where shareholders can force change rather than wait forever for it.

His opening slide read “Japan is back.” The Nikkei closed the night before at 67,640, well above its 1989 bubble peak, and Fischer credited a decade of governance reform for shifting the mood from accepting a sub-5% return on equity and a price under book value toward holding boards accountable. The timing matters, because most Japanese companies hold their annual meetings in a single late-June window that hands an activist a hard deadline.

See: Hedge Fund Management is Not a 9-5 Job: Interview With Oasis Management’s Seth Fischer

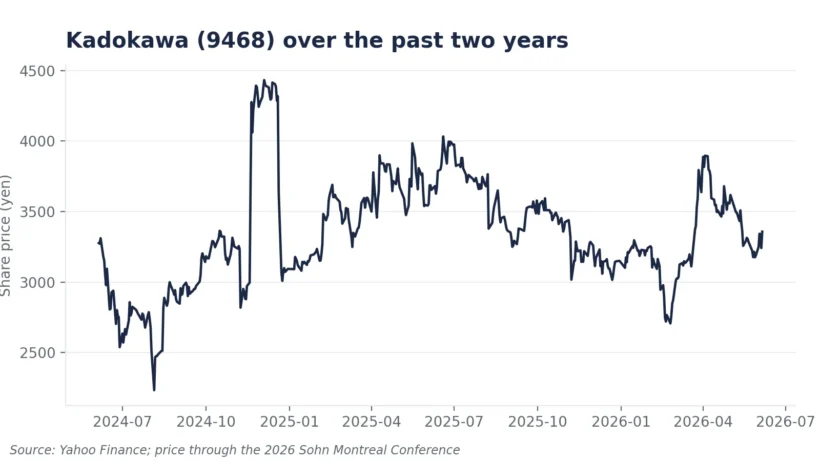

Rather than pitch one stock, Fischer laid out seven names Oasis is engaged with, each a business he says has a real franchise buried under poor leadership, over-diversification, or entrenched directors. He thinks the upside in some runs past 100% if the boards change. The thesis: these companies are cheap because they are badly run, and Oasis intends to do something about it before the meetings close.