David Einhorn’s Q1 2026 letter to investors from his Greenlight Capital. See the full PDF here below. First brief highlights:

Read more hedge fund letters here

- Longs / new positions / winners: ACHC, DHT, CNR, VSNT, CROX, SLM, Brighthouse Financial, Fluor, Green Brick Partners, SOFR

- Losers / exited: GPK, KD/Kyndryl, Global Payments, Warner Bros., Lebanese sovereign debt (yes you read that right)

- Cover letter with performance figures

- Iran war scenario analysis

- Q1 attribution table (longs/shorts/macro)

- All stock write-ups (ACHC, DHT, CNR, GPK, KD, VSNT, CROX, SLM)

- Largest positions at quarter-end

See the full letter below.

The Greenlight Capital funds (the “Partnerships”) returned 6.5% in the first quarter of 2026, net of fees and expenses, compared to -4.4% for the S&P 500 index.1

“It’s tough to make predictions, especially about the future.” – Yogi Berra

Fundamentally, we are in the business of making predictions. When we buy or sell short a stock, we believe the prospective reward is worth the perceived risk. Every trade is a debate with someone taking the other side, and every position reflects our prediction of how that debate will resolve.

Read more hedge fund letters here

When Greenlight launched thirty years ago, we concentrated almost entirely on predicting individual stocks. We were trained in securities analysis and believed we could figure out what securities were worth, when they were mispriced, and what the market misunderstood. When we believed we had genuine insight and the scales were tipped in our favor, we invested.

Over time, we realized we needed to look beyond the microeconomics of individual companies. The great financial crisis taught us that we needed to consider the bigger picture – the macroeconomy. So, we evolved. We now think ‘top-down’ in addition to ‘bottom-up.’ Now, when we have a clear basis for a macroeconomic prediction, we invest directly in macro instruments.

From time to time, extraordinary world events force us to study new areas that extend well beyond securities or economic analysis, where we have no previous experience or relevant expertise. For example, after 9/11 we had to assess whether a series of terrorist attacks and the resulting security needs would cripple the economy. More recently, in 2020 we had to navigate a global pandemic, the potential transmission of a deadly disease, the societal reaction and the outlook for a vaccine.

Such is the case with the current war in Iran. As we see it, the important questions for the market are: How will the war progress? Will the current two-week ceasefire lead to peace or resumed fighting? How long will the Strait of Hormuz be closed? What will happen to the price of oil, and how will that affect the economy? If we could answer these questions, we could predict how the markets would respond and position the portfolio accordingly.

Unfortunately, we don’t have a clue.

A year ago, we quipped about President Trump: “The news cycle changes very rapidly. If you like the latest news, enjoy it for two hours. It will change. If you don’t like the news, wait two hours, it will change.” At the time, we meant the news cycle went from one topic to the next. We didn’t mean constant flip-flopping on the most important issues for the market.

One moment President Trump demands “unconditional surrender.” The next he says we’ve completed most of our objectives. One moment he demands regime change. The next he says regime change already happened. One moment he threatens to bomb Iran back to the “Stone Age.” The next he says we have already destroyed almost all the relevant targets. One moment he says opening the Strait of Hormuz is of little concern and not America’s problem. The next he says, “Open the F*ckin’ Strait, you crazy bastards, or you’ll be living in Hell – JUST WATCH!”

Setting aside the widely discussed rumor that his statements are designed to move financial markets after being front-run by his family or close associates, we have no idea what he is actually going to do. Maybe he doesn’t either. We liked this recent meme:

More seriously, we do wonder what the purpose of all this flip-flopping is. If President Trump wants Iran to negotiate a settlement, we are confused why he would routinely signal he might withdraw at any moment. America has developed a reputation since Vietnam that its enemies can simply outlast us. Surely, threatening to “declare victory and go home” does not inspire the enemy to rush to the bargaining table. It also undermines the credibility of the more serious- sounding threats.

The recently agreed ceasefire appears to have been driven by President Trump determining that if we destroyed Iran’s bridges and power infrastructure, the retaliation would bring an unacceptable cost. Iran reluctantly agreed to the ceasefire under Chinese pressure after Trump acknowledged that Iran’s 10-point peace plan could be the basis for negotiations.

Since we cannot figure out what will happen, we must consider multiple scenarios. Some of the possibilities include:

- The current peace talks are successful, and both sides find enough to declare victory. The Strait of Hormuz reopens either with or without tolls. The markets can get back to wondering whether the rules for index inclusion of new issues with small floats can be influenced to create so much passive demand that SpaceX can successfully IPO at any valuation.

Read more hedge fund letters here

- The talks break down, but hostilities do not resume. The situation essentially freezes as things stand or they resume at a lower intensity. For example, rather than attacking Iran, the U.S. could try to blockade Iran’s oil exports.

- The talks break down and hostilities resume. In one scenario the U.S. military wins quickly. The Iranian regime collapses and the U.S. Navy restores the Strait’s shipping lanes. In another scenario, the war resumes without resolution. Iran suffers enormous infrastructure damage and loses its ability to export oil. The Gulf States and Israel suffer from retaliation and the region’s ability to produce and transport energy, fertilizer and other goods is significantly impaired.

- None of the above. Something else happens that we can’t foresee.

Conflict escalation would result in many open questions including:

- Will civilian infrastructure, including desalination plants, suffer sufficient damage to leave portions of the region uninhabitable?

- Could Iran carry out a significant terrorist event on American soil?

- Will other countries join the conflict?

- Will other actors use the chaos to pursue mischief elsewhere? North Korea vs. South Korea? China vs. Taiwan?

Similarly, successful resolution would result in many open questions including:

- How long will it take to reopen the supply chain? Are intermediate-term shortages already baked in? Has the price of energy been permanently elevated? Has the damage already incurred baked in a new round of inflation? Will higher energy prices lead to a slowdown or even a recession?

- How will the Gulf States adjust to the new geopolitical realities? Will oil continue to be priced primarily in U.S. dollars?

- Will the U.S. maintain influence in the Middle East? What are the implications for the dollar, U.S. Treasuries and gold?

Obviously, the implications of these different scenarios on markets are wide-ranging.

Given that we don’t know what will happen, how are we approaching this? Our first step has been to assess how the market has already priced in (or not) the various possibilities.

Our assessment is that most investors are positioned primarily for a favorable resolution. If you told us that war would break out with Iran, the Strait would be closed, there would be significant damage to some energy infrastructure and the price of oil would rise above $100, we would have expected a much deeper equity market correction. With the announcement of the ceasefire, the market has already recovered its decline since the war started, even though energy prices remain elevated and the uncertainty described above remains.

However, investors may be reasoning that headlines reading “Bombs start falling” must eventually be replaced with headlines reading “Bombs stop falling.” And who wants to sell before that happens?

In recent years, investors have been conditioned not to sell into bad news. If you sold COVID, there was a near perfect V-shaped bottom. In fact, it was more of a checkmark shape. Sellers lost badly. If you sold in the summer of 2022 or the fall of 2023, the same thing happened, but less dramatically. If you sold the Liberation Day scare, it was like COVID – another checkmark recovery. If you sold all of those, you are probably no longer managing money professionally. If you sold all of those as an individual, you are probably out of the market.

Who is left? Passive investors and people and institutions that have learned not to sell into declines.

Even the most cautious are investing with a Sammy Hagar inspired mentality: one foot on the brake and one on the gas. Thus, the market has rallied furiously on any presidential tweet that the U.S. might withdraw, news stories that the Iranians are willing to consider negotiating and, of course, the ceasefire announcement. Nobody wants to miss the V- or even the checkmark- shaped recovery.

As the conflict started, we were positioned with relatively low gross and net exposures. From our perspective, the market was already very expensive. We have reacted by changing very little. We have traded around index hedges and added a long position in October oil futures, which has only moved up modestly, as there is widespread anticipation that there will not be an enduring shortage.

It probably won’t surprise anyone that we are again putting capital preservation at the top of our priorities. With so little downside priced in, we are willing to risk missing out on a possible recovery to position ourselves to play more offense, should one of the downside scenarios materialize.

We had a strong start to the year with longs, shorts and macro each contributing positive returns and positive alpha, as shown in the table below:

Gross Contribution Alpha2 Longs 1.5% 6.7% Shorts 4.8% 2.2% Shorts (index) 0.7% -0.1% Macro 1.5% 1.5% Total (Gross) 8.5% 10.3% Total (Net) 6.5%

Given all the geopolitical chaos in March, it is hard to remember that there were two months preceding it in the quarter.

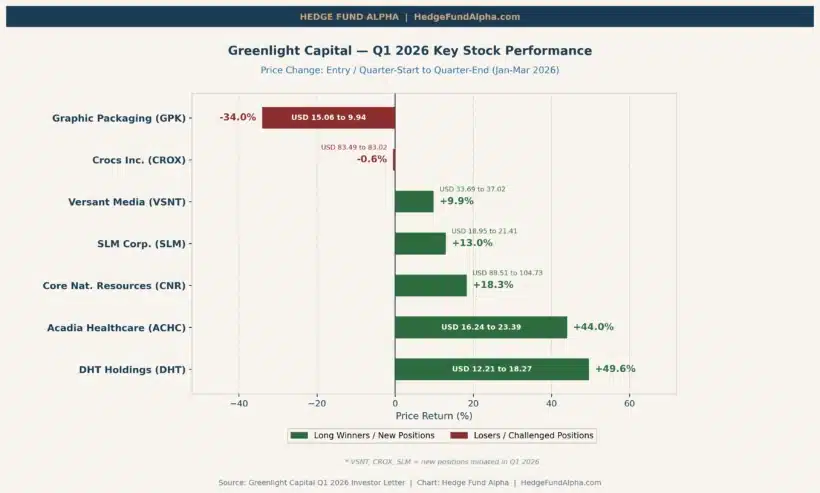

Our significant winners in the quarter were gold, Acadia Healthcare (ACHC), DHT Holdings (DHT) and Core Natural Resources (CNR). Our biggest losers were SOFR futures, Kyndryl Holdings (KD) and Graphic Packaging (GPK).

For the first two months of the quarter, the de-dollarization thesis gained traction. Gold started the year at $4,339 per ounce and peaked in late January at $5,595. This led to large gains for us in both physical gold and binary gold call options. As the calls moved into the money, they began to behave more like short out-of-the-money puts. As a result, we sold most of the options and rolled some of them forward, taking profits in the process. This allowed us to preserve the majority of our gains in gold, even as it declined later in the quarter in response to the war. We continue to hold our gold position, including a much smaller position in binary call options.

ACHC is the leading pure-play behavioral healthcare clinic operator in the U.S. After peaking near $90 in 2022, the stock came under heavy pressure in late 2024 following a New York Times investigation that revealed poor and sometimes abusive treatment of patients. While we bought a small position at the time around $51 per share, this proved to be only the beginning of ACHC’s challenges. Due to an overly aggressive expansion strategy and an inability to manage its patient ramp, ACHC had occupancy challenges that weighed on results, while litigation expenses were growing. ACHC shares ultimately bottomed out at around $11 in January.

Our work suggested the problems were entirely management-related and that ACHC’s asset quality is strong. Early this year we increased our position, believing that a leadership change was probable. Ultimately, our average entry price for what is now a top 5 position is $16.24 per share.

In January, the company replaced its CEO, bringing back the former CEO who ran the company successfully from 2018 to 2022. The returning CEO is among the most well-regarded and capable operators in the industry. With this injection of confidence and competence, the shares recovered to $23.39 by the end of the quarter. Should the company achieve stabilized occupancy, we believe it would earn over $3 per share.

DHT advanced from $12.21 to $18.27 per share during the quarter. The company owns and charters out Very Large Crude Carriers (VLCCs). Even prior to the war, VLCCs were in short supply, with day rates rising to about 500% of the long-term average level. The company pays out its current earnings as a dividend, and at these elevated charter rates, we expect the dividend to rise from $0.74 to $3.50 per share this year.

CNR stock went from $88.51 to $104.73 during the quarter. More than all the gain came after the war began. As the war disrupts natural gas supply on a global basis, demand for coal increases. It is too soon to quantify the positive impact for CNR.

We are long SOFR futures with the view that the new Chairman of the Federal Reserve will be more supportive of rate cuts. As the war started and oil spiked, the market became doubtful that the Fed would be able to cut rates this year, and for a little while was even pricing in a rate hike. This resulted in losses on this position in March and for the quarter.

We nonetheless persist. We believe that an oil price shock is a headwind to growth and a threat to jobs and that the new Chairman will change the Fed framework from “data dependency” – which focuses on backward-looking economic data – to a forward-looking view. Historically, oil price shocks have preceded many recessions. We believe the new Chairman will lower rates to try to prevent a recession.

We owned KD for over four years. During most of that time, the company executed a successful turnaround after its spin-off from IBM. Recently, it has become more challenging to win new business. As a result, the shares have made a full round trip from the low double digits to $40 a share and back. Fortunately, we took some profits at higher prices. Given the difficult environment, including threats from AI, as well as an SEC investigation into the company’s accounting and cash management practices and the departure of its CFO, we exited the balance of our position this quarter. Ultimately, we earned a 17% IRR.

GPK shares fell from $15.06 to $9.94 during the quarter. The company failed to meet earnings expectations and lowered future guidance, with costs for its newly built paper mill coming in well over budget, and the competitive environment proving to be unusually challenging. The company fired its experienced, well-regarded CEO and replaced him with a CEO who recently presided over a massive disappointment at his prior company. As yet, the new CEO has not articulated a clear strategy. Shareholders have been understandably grumpy and the stock has suffered. We believe the shares are extremely cheap relative to a reasonable mid-cycle performance.

We initiated a medium-sized new position in Versant Media Group (VSNT) and small new positions in Crocs, Inc. (CROX) and SLM Corp. (SLM).

We established our position in VSNT at an average price of $33.69 per share. VSNT is a recent spin-off from Comcast and owns cable channels like MS NOW (formerly MSNBC), CNBC

and USA Network, along with other non-Pay TV assets including GolfNow and Fandango. While the legacy cable business faces ongoing cord-cutting, over 60% of its programming is tied to live news and events, which we believe is more resistant to subscriber losses than other entertainment categories. Additionally, the company’s non-Pay TV revenues are growing and now represent nearly 20% of total revenues.

Following the spin-off, shares declined as Comcast shareholders sold stock they received, and index rebalancing forced additional selling when VSNT was removed from major indices. These dynamics left the shares trading at less than 4x adjusted EBITDA and an implied cash flow yield that supported the company’s ability to return nearly its entire market cap within four years. VSNT ended the quarter at $37.02 per share.

CROX is a global footwear company best known for its iconic clogs. It is a well-run business with industry-leading margins and a 10-year annualized organic sales growth rate of 12%. Last year, a decline in U.S. sales raised existential concerns about the core brand, which we believe were overblown. While consumer preferences have shifted in the U.S., over half of core Crocs brand sales now come from international markets, which continue to grow at a strong pace. We also expect U.S. declines to moderate as comparisons normalize following last year’s inventory clean-up actions. We established our position at an average price of $83.49 per share, or about 6x our 2026 EPS estimate. The company has directed most of its free cash flow to buybacks, and we expect annual repurchases of over 10% of the outstanding shares going forward. CROX ended the quarter at $83.02.

SLM is the largest originator of private student loans in the U.S. The stock has declined due to concerns around AI-driven displacement of white-collar jobs and its impact on delinquencies. We established our position at an average price of $18.95 per share, or about 7x and 4x our 2026 and 2028 EPS estimates, respectively. It is inherently difficult to predict the influence AI will have on employment this early in the adoption curve, but over time, we expect workers to adapt and reskill to match the evolving job market. Nearly 90% of SLM’s loans are cosigned, typically by a parent or grandparent, mitigating credit risk. We also see an opportunity for significant growth in graduate student lending as the federal government exits the market following provisions in the One Big Beautiful Bill Act. SLM has been actively repurchasing shares, including a recently completed accelerated share repurchase program totaling about 5% of the outstanding shares, and we estimate capacity to repurchase approximately 30% of the outstanding shares over the next three years. SLM ended the quarter at $21.41.

In addition to exiting KD, we exited:

Global Payments at around our cost, as further diligence raised questions about what the company is classifying as organic growth. • Lebanese sovereign debt with a 66% IRR over a 1-year holding period, as it became more likely that the country would resolve its default. • Warner Bros. Discovery with a solid gain over a 2-month holding period, as we believe that the auction for the company has reached a resolution.

At quarter-end, the largest disclosed long positions in the Partnerships were Acadia Healthcare, Brighthouse Financial, Core Natural Resources, Fluor and Green Brick Partners. The Partnerships had an average exposure of 82% long and 46% short.

“Come to TACO, TACO, TACO, TACO, TACO, TACO, TACO, TACO, TACO, TACO, TACOOOOH BELL!” – Memorable ad jingle from the 1970s

Best Regards,

Greenlight Capital

Read the full investor letter here.