Black Bear Value Fund commentary for the second quarter ended June 30, 2025.

Read more hedge fund letters here

“I’m not telling you it’s going to be easy – I’m telling you it’s going to be worth it.” – Art Williams

To My Partners and Friends:

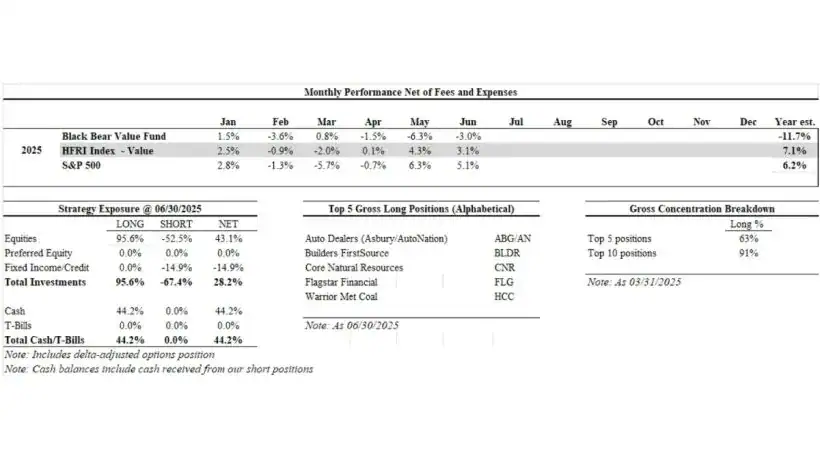

- Black Bear Value Fund, LP (the “Fund”) returned -3.0% in June, -10.5% in the quarter and -11.7% year-to-date.

- The S&P 500 returned +5.1% in June, +10.9% in the quarter and +6.2% year-to-date.

- The HFRI Index returned +3.1% in June, +7.7% in the quarter and +7.1% year-to-date.

- We do not seek to mimic the returns of the S&P 500 and there will be variances in our performance.

Note: Additional historical performance can be found on our tear-sheet.

Although our Partnership has a long-term mindset, I am realistic that short-term underperformance and in particular drawdowns can be a source of consternation. Note that as we sit here in early July the portfolio has partially rebounded as a few of the catalysts described later started to come to fruition. The portfolio is a coiled spring, with lots of bad news/expectations priced into what we own, and good news/magical thinking priced into what we are short. Many of our businesses are experiencing hard catalysts in the coming 6-18 months which will unlock lots of cash and value (more on this below).

I generally reserve a more fulsome portfolio discussion for year-end but feel it’s appropriate to have a more detailed Q2 letter. I would encourage you to read the Company updates, even if they are long held positions, as I discuss the ideas in more detail. I am including the business performance thru the Companies latest earnings release as well.

A little more than half of our negative mark to market is a result of our short portfolio. In the 2nd quarter, many money-losing companies went up sharply. This is temporary. We’ve been through this before and ultimately the short book has helped us make up ground in dramatic fashion. As a reminder in 2022 when the market was down 18%, we were able to report a +12% year in large part due to our short portfolio. Our short portfolio will help us again even though the temporary mark to market is aggravating.

Several of our Companies have hard catalysts in 6-18 months which will produce a large amount of cashflow. Management teams can either buy back stock, pay dividends or utilize in another accretive manner. Many of our companies are already experiencing trough conditions and are priced as if this will continue ad infinitum. Things will improve and along with it sentiment. As painful as mark-to-market losses are, we own Companies that are proactive in buying in cheap stock. When sentiment improves there is less stock available, and prices move up a lot (See BLDR or AN historical performances).

Here is a rough summary of some of our 2025-2026 catalysts:

- Core Natural Resources: One of their larger met coal mines is offline and will return.

- Warrior Met: The Blue Creek development will be completed, and the Company will gush cash

- Flagstar: As the turnaround continues progressing the Bank will get back to profitability and look better than their competition

- Franklin Street Properties: A distressed REIT we own that has several activists involved (one on Board) – is currently working with Bank of America on a strategic review.

- Leon’s Furniture: Leading Canadian furniture retailer (70% owned by founding family) that is spinning off real estate that’s equal to near the 2/3 of the entire Company market cap.

Top 5 Businesses We Own (Alphabetical)

Auto Dealers: Asbury Automotive Group Inc (NYSE:ABG) & AutoNation Inc (NYSE:AN)

Asbury Group and AutoNation operate auto dealerships across the United States. The strength of the model comes from the back of the house in parts and services where more than 50% of the profits come from. Auto retailers are resilient businesses that generate strong free cash flow even in soft markets. ~90% of auto dealerships are privately owned providing a long-term runway for consolidation and growth. There are scale advantages to being a larger public dealer (access to capital for M&A, ability for strong parts/service business as cars become more complex, lower overhead costs, brand equity). The businesses are priced as if there will be no growth.

In the shorter term tariffs will increase the cost of an automobile (how much is hard to say), reducing the affordability for both new and used cars (holding all else equal). Some of this will be mitigated by a highly variable component in the wage expense. Some damage may also be mitigated by increased activity in the Parts & Service division. The impact of tariffs could take some time to be felt and its uncertain if there will be tax credits/interest deductibility to lessen the pain on American consumers.

Asbury Automotive Group reported a solid, though slightly softened, financial performance in Q1 2025. Revenue declined ~1% year-over-year, with gross profit decreasing 3%. Parts & service remained a bright spot, delivering a same-store gross profit increase of ~5%, driven by strong customer-pay demand (Parts & Service). Management noted resilience amid tariff uncertainty and weather disruptions and reaffirmed its pending acquisition of Herb Chambers Automotive Group, expected to close by mid-2025.

ABG should be able to earn $20-$30 in free-cash flow per share in a “normal” year. Additionally, they now provide warranty and service contracts in-house (TCA). This business is worth ~$30-$40 per share. At a quarter-end price of $239 and accounting for a $35 TCA value, we own ABG at ~10-15% free-cash-flow yield. This compares to the S&P500 which is ~3-4% free-cash-flow yield.

AutoNation reported strong Q1 2025 results, with revenue climbing approximately 3% year-over-year driven by a 7–10% increase in same-store new vehicle sales. Gross profit increased about 2% including a record $568 million in after-sales profit as margins expanded by roughly 140 basis points. Used-vehicle profitability also surged: gross profit per unit rose about 13% to $1,662, and total used-vehicle profit jumped around 12% The Customer Financial Services arm grew ~5–6%, with improved per-unit returns. Capital deployment totaled ~$370 million, including $225 million in share repurchases (reducing shares by ~3%) and $70 million in two store acquisitions. Management highlighted resilient market dynamics, improved inventory efficiency (days’ supply down ~14%), and continued diversification across revenue streams—reinforcing confidence in AutoNation’s robust, multi-channel automotive retail mode.

AN should be able to earn $15-$20 in free-cash flow per share in a “normal” year. AN also has a smaller lending business that’s conservatively worth ~$8 a share and an AutoNation USA standalone used-car business which is worth ~$15 per share. At a quarter-end price of $199 and accounting for $23 in value from the lending business and AN USA we own AutoNation at 9-11% FCF yield. This compares to the S&P500 which is ~3-4% free-cash-flow yield.

Builders FirstSource, Inc. (NYSE:BLDR)

There is a structural shortage of housing in the USA. Higher mortgage rates reduce the supply of existing home supply as homeowners are locked into low-rate mortgages. As we have seen in recent history, the overall pie of housing activity may shrink, with new homebuilders capturing an increasing share of home sales. Homebuilders can buy-down the mortgage to a lower rate and accept a lower, yet still healthy margin on the home sale.

BLDR is a manufacturer and supplier of building materials with a focus on residential construction. Historically this business was cyclical with minimal pricing power as the primary products sold were lumber and other non-value-add housing materials. Since the GFC, BLDR has focused on growing their value-add business that is now 40%+ of the topline. The company has modest leverage and has been using their abundant free-cash-flow to buy over 45% of their stock in the last 33 months.

Builders FirstSource experienced a sharp downturn in revenue, profit, and cash flow in Q1, reflecting broader market softness. However, the company delivered a modest earnings surprise, maintained strong liquidity, and continued to invest in operational efficiencies and shareholder returns signaling confidence in its long-term strategy despite current headwinds.

Of most importance, Q1 is one of their slowest quarters (winter is slow for homebuilding) and BLDR maintained its 2025 outlook, targeting $16.05–17.05 billion in net sales, gross margins of 29–31%, adjusted EBITDA of $1.7–2.1 billion, and $800–1,200 million in free cash flow (a 6-9% free cash flow year in a trough year is much improved compared to past slowdowns).

The company has sustained higher gross margins as they have gained scale. I estimate normalized free-cash-flow per share to be $10-$15 per year implying a free-cash-flow yield of 9-13% with no growth priced in. The reality is due to the housing shortage coupled with acquisitions from smaller competitors; there is a long-term tailwind providing growth. Additionally local governments are beginning to loosen red tape for home construction which should help.

Core Natural Resources Inc (NYSE:CNR)

Core is the result of the merger between Consol and Arch Resources. As a combined entity they are one of the leading producers of metallurgical coal (steel) and thermal coal (energy). The Company is heavily dependent on exports so retaliatory tariffs would be damaging. At the same time, there has been a reduction in global capacity so many countries may not have much choice, especially if they need higher quality coal.

Following its January 2025 merger of Arch Resources and Consol Energy, Core Natural Resources reported Q1 2025 revenue slightly outpacing revenue forecasts. The company allocated $106.6 million to investors via buybacks and dividends and bolstered financial flexibility by refinancing its revolving credit facility. Management emphasized early merger synergies, robust free cash flow, and prudent capital deployment through shareholder returns and site-led efficiencies.

Met coal demand is projected to climb for the next 25 years, driven by the economic development and urbanization in India and the rest of Southeast Asia. ~60% of the world’s population lives in Asia, where met coal demand is centered and where local sources are limited. Over the coming years demand will likely outstrip supply, leading to higher prices. There has been a severe lack of investment in met coal due to ESG concerns with investment peaking in 2014.

One of Core’s met coal mines experienced a fire and will re-open later in 2025. Due to this and lower met coal pricing, Core should generate somewhere between $250-$550MM in free-cash-flow in 2025 (with some upside from merger synergies). This equates to ~$5-$10 in free-cash-flow per share in a weaker year vs. a $70 stock price per (a 7-14% unlevered yield). In a more normal year, when pricing gets back to average and production comes back online, CNR should generate $500MM-$1.0BB ($9-$19 in FCF per year or a 13-27% mid-cycle unlevered yield.

As a reminder this is a Company with a fortress balance sheet and is one of the cheapest producers in the market. While short-term pain hurts all Companies, they can be major long-term beneficiaries.

Warrior Met Coal Inc (NYSE:HCC)

Warrior Met Coal is a leading metallurgical coal producer (coal used to steel production). Currently the bulk of HCC’s FCF is being invested in a capital project that will be concluding this year. Once the business winds down their investment period they will gush cash.

In Q1 2025, Warrior Met Coal saw revenue down 40% year-over-year due to compressing met coal prices. Despite a 10% production increase and tight cost control, negative free cash flow of $68 million reflects heavy investment in the Blue Creek mine. Liquidity remains robust at $617 million. Management maintained its full-year guidance, emphasizing the strength of contracted sales, cost discipline, and continued advancement of the Blue Creek project amid market headwinds.

HCC’s existing mines should generate $100-$350MM in annual free cash flow (assuming lower for longer met coal prices). Blue Creek development is wrapping up by the beginning of 2026 and at mid-cycle should generate $100-$500MM in additional free cash flow. The combined assets should generate $200MM-$850MM in free cashflow with non-heroic pricing and volume assumptions. This equates to ~$4-$16 in annual per share cash generation vs. a price of ~$46 or a 9-35% unlevered annual free-cashflow yield.

2026 should be a sea-change in their free-cash-flow generation.

Flagstar Financial Inc (NYSE:FLG)

Flagstar Financial is the former New York Community Bank (a mashup of Flagstar Bank, New York Community Bank and assets from Signature Bank). Like our SHORT investments in Silicon Valley Bank and First Republic, FLG had a hole in their balance sheet (from soured multifamily and office real estate vs. long-duration securities). That is where the similarities end.

FLG raised over $1BB in additional capital, led by former Treasury Secretary Steven Mnuchin. They revamped the management team and brought in a superstar CEO in Joseph Otting. They have reviewed nearly all the loans on the books, sold off non-core assets, raising additional capital and are focused on delivering a narrowly-focused, well-capitalized boring regional bank. In this case boring is good. Importantly, they have taken a conservative view of their loan book and a large credit reserve. This contrasts with several bank/private credit lenders we are short who have taken minimal reserves.

In Q1 2025, Flagstar Financials’ net interest margin stabilized at 1.74%, and expense controls reduced adjusted non-interest costs by over 20% annually. Strong loan growth (commitments up 32%) and ongoing credit improvement signal operational momentum, while the CET1 ratio of 11.9% and disciplined exposure reduction in commercial real estate reinforce financial stability. With a clear plan focused on cost savings and strategic lending, Flagstar is on track to return to profitability by the end of 2025.

At quarter-end the bank was trading at ~60% of a conservatively marked balance sheet. This is in contrast with similar banks (who are NOT conservatively marked) trading at 140-160% of their tangible book value. FLG should complete working thru the bulk of their issues by the end of 2025 and approach “normal” during 2026. Given the conservative nature of the management team, I wouldn’t be surprised if it happened sooner. At these prices the downside seems minimal and could see this business up 50-150% over the next 1-3 years as it is more appropriately valued.

Concluding Thoughts

Animal spirits seem to be in vogue again. I understand that it’s unpleasant to experience a mark to market loss, but these have historically proven to be temporary. Our returns are lumpy in nature due to our concentration. We will wind up making money on our shorts as the fundamental weakness in these businesses are exposed as tariff impact and a slowing economy become more evident. Our long investments are long-term beneficiaries of weak share prices and can take advantage of buying back stock. We own a group of businesses that have a lot of bad news priced in at enormous discounts to overall elevated market multiples. Time is our friend.

We know what we own and are sober/objective in our reasoning and will stand to do well in the coming years. Please reach out if the Fund is of further interest.

Thank you for your trust and support.

Black Bear Value Partners, LP

786-605-3019/646-821-1854

www.blackbearfund.com