FPA Paramount Fund commentary and webcast slides for the fourth quarter ended December 31, 2018.

Q4 hedge fund letters, conference, scoops etc

FPA Paramount Fund 4Q18 Webcast Audio

FPA Paramount Fund 4Q18 Commentary

Dear Fellow Shareholders,

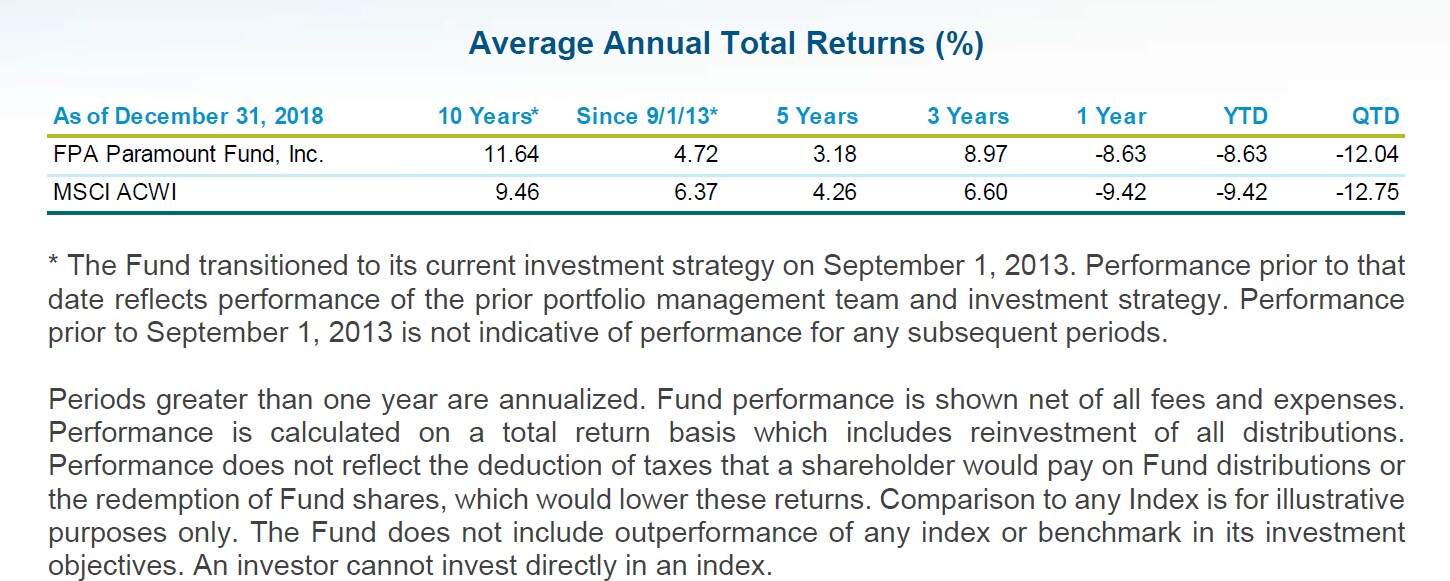

During the fourth quarter of 2018, the FPA Paramount Fund (the “Fund”) declined 12.04% (in U.S. currency) compared to a decrease of 12.75% for the MSCI ACWI (Net) (the “Index”). For the full calendar year, the Fund fell 8.63% (in U.S. currency) compared to a decrease of 9.42% for the Index.

While the fourth quarter results were stronger than the Index, we continue to believe short-term performance is not the best way to judge investment results. As value investors, we seek to buy businesses at a discount. Stock prices can, and often do, decline after purchases. We also know that market sentiment toward an industry, or even a specific company, often shifts significantly from one year to the next. It typically takes several years for discounts to our estimates to unwind. That is why we advocate evaluating the Fund’s performance over longer periods, ideally over a market cycle.

Key Performers

The biggest disclosed performance detractors in the quarter were Sulzer, Capgemini and Ryanair.1 Sulzer, which was our second-worst-performing holding this quarter, declined 33.89% (in U.S. currency).2 Based in Switzerland, Sulzer manufactures pumps and other machinery for energy, chemical and power generation customers. Despite strong reported results for the period, declining crude oil prices appear to have caused the market to worry about future prospects. Based in France, Capgemini is a leading global information technology consulting, outsourcing and professional services company. Concerns about a slowdown in corporate technology spending weighed on the shares. Based in Ireland, Ryanair is Europe’s leading passenger airline. Issues involving insufficient air traffic control capacity and the transition to union representation for its employees have disrupted flight schedules. Rising fuel prices have also weighed on profitability.

Empire, Hypera and Magazine Luiza were the top performance contributors for the quarter.3 Based in Canada, Empire is a leading grocery store operator and wholesale food distributor whose results continue to improve under a relatively new management team. Based in Brazil, Hypera is one of the country’s leading pharmaceutical companies. Based in Brazil, Magazine Luiza is a leading retailer, operating an e-commerce platform and physical stores.

Portfolio Activity

We made several new purchases in the fourth quarter, including Magazine Luiza, Notre Dame Intermedica (“Intermedica”) and Stroeer. Based in Brazil, Intermedica is a leading health insurer and operator of hospitals and other health care facilities. Stroeer, based in Germany, is a leading provider of out-of-home advertising solutions with around 300,000 sites across the country. The group also operates a large portfolio of German-language websites, and through several acquisitions, is also a provider of direct marketing services.

We also sold several companies, including Empire, Alicorp, Twenty-First Century Fox (“Fox”), and Frutarom. As previously mentioned, Empire is a leading grocery store operator and wholesale food distributor, based in Canada. Based in Peru, Alicorp is the country’s leading producer of food, home and personal care products including margarine, pastas, mayonnaise, detergent and hair care products. Empire and Alicorp’s share prices had increased significantly and converged toward our estimate of intrinsic value, so they no longer offered the margin of safety we require.to remain invested. We continue to view both companies as well-run, high quality businesses that we would consider owning again at the right price.

Merger activity caused us to sell Fox and Frutarom. Based in the U.S., Fox operates a global media business. During the fourth quarter of 2017, the company announced an agreement to sell its film and TV studios and some of its TV networks to Disney. Based in Israel, Frutarom is a leading producer of key ingredients for food and beverage products. The company was acquired by International Flavors and Fragrances, a large U.S. peer. Finally, since the merger between Essilor and Luxottica has closed, we are now holders of EssilorLuxottica (“Essilor”) stock. Based in France, Essilor is a leading producer of eyeglass lenses. Based in Italy, Luxottica is a leading producer of frames and sunglasses.

Portfolio Profile

We owned 44 disclosed positions as of December 31, 2018. This is within the range of the number of businesses we would expect to own at any given time.

Most of the Fund’s positions are in large-cap companies (with a weighted average capitalization of approximately $88 billion). However, we do not consider a company’s size to be a relevant criterion from an investment perspective. Reflecting a median capitalization of approximately $16 billion, we are invested across a wide range of market capitalization sizes, including several businesses that are considered megacaps.

At quarter end, most of the Fund’s assets were invested in companies domiciled in Europe (about 54%). The United States represented about 22%, with Asia-Pacific about 4%, and the balance in other regions and in cash. Where a company is domiciled is largely irrelevant to us, however, since many of our holdings are large companies that conduct business on a global scale. That means they often generate significant amounts of their cash flow outside their home countries, rendering traditional country classifications less useful.

We thank you, as always, for your confidence, and look forward to continuing to serve your interests as shareholders of the FPA Paramount Fund.

Respectfully submitted,

Gregory Herr

Portfolio Manager

Pierre O. Py

Portfolio Manager