Owens & Minor, Inc. (OMI) is a healthcare logistics company with a market cap of ~$1 billion.

[timeless]

Q2 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

What stands out about the company is its absurd valuation. It is currently trading for a share price not seen since the beginning of 2004.

Owens & Minor shares are down 63% since highs reached in 2016. Meanwhile, adjusted earnings-per-share have declined 21% (using expected 2018 adjusted EPS of $1.45). Clearly, the stock has sold off more than its earnings have declined.

Owens & Minor recently reported its 2nd quarter results on August 7th. Revenue grew 8.5% and adjusted operating income increased 12.6% versus the same quarter a year ago, while adjusted earnings-per-share declined from $0.43 to $0.32. The company also reported adjusted EPS guidance of $1.45 for fiscal 2018, which is significantly below our previous estimate of $2.00.

Is Owens & Minor still a buy, or is it time to sell?

We are reaffirming our buy recommendation on Owens & Minor. The company’s management is expecting 10%+ adjusted earnings-per-share growth in 2019, and we expect further strong growth beyond 2019. And, the company is extremely undervalued at current prices. Overall, we expect 20%+ annualized total returns from Owens & Minor at today’s prices.

For current shareholders now is not the time to sell. The stock still ranks as a strong buy. For more on Owens & Minor, see our new Sure Analysis report here.

Owens & Minor (OMI)

Key Metrics

: Still A Buy? 1")

Overview & Current Events

Owens & Minor is a healthcare logistics company that provides packaged healthcare products for hospitals and other medical centers. The company has a market capitalization of $1.1 billion and distributes ~220,000 different medical and surgical supplies to ~4,400 hospital systems worldwide. Owens & Minor has increased its dividend for 19 consecutive years.

In early August, Owens & Minor reported (8/7/18) financial results for the second quarter of fiscal 2018. In the quarter, the company generated consolidated revenues of $2.46 billion, which represents an 8.5% increase over the $2.27 billion generated in the same period a year ago. Contributors to this strong revenue growth include $128 million from the acquisition of Byram Healthcare and two months of revenue contribution from Halyard Health’s Surgical & Infection Prevention (S&IP) business. Moving down the income statement, Owens & Minor generated adjusted consolidated operating income of $46.6 million, a 12.6% increase year-on-year. Adjusted net income was $19.4 million, or $0.32 per share, which compares poorly to the $0.43 in earnings-per-share generated in the second quarter of 2017.

Owens & Minor also provided some very disappointing guidance for the remainder of the fiscal year. The company now expects to generate adjusted earnings-per-share between $1.40 and $1.50. This is well below our prior estimate of $2.00. We have updated our 2018 and 2023 earnings-per-share estimates accordingly. Likely due to this weak guidance, Owens & Minor’s shares fell by as much as 17% on the first trading day following the earnings release.

Per-Share Growth

: Still A Buy? 2")

Owens & Minor’s earnings-per-share are currently lower than they were in 2008. With that said, this does not tell the whole story. Sales per share and free cash flow per share have both compounded at ~3% per year during that time period. Owens & Minor has recently completed a number of promising acquisitions that should fuel its growth for the foreseeable future. Last year, the company closed (8/1/17) on the acquisition of Byram Healthcare, a $380 million purchase that generate $450 million in sales for the company and be earnings accretive in 2018. More recently, Owens & Minor announced (11/1/17) the acquisition of Halyard Health’s surgical & infection prevention (S&IP) business for $710 million – the largest acquisition in Owens & Minor’s history. The transaction closed in 1Q2018. Earnings should rebound next year as these two acquisitions begin to impact the company’s financial results. Beyond that, we believe Owens & Minor should compound its earnings in the high single digits – around 8% per year – moving forward.

Valuation Analysis

: Still A Buy? 3")

Using the midpoint of Owens & Minor’s new 2018 financial guidance, the company is trading at a price-to-earnings ratio of 10.7. If the company’s valuation can revert to 18 times earnings (near its 10-year average of 18.2 times earnings) over the next 5 years, this will add 10.9% to the company’s annualized returns during that time period. Undervaluation has also lead to a remarkably high dividend yield. Owens & Minor’s 6.7% dividend yield has a comparably low payout ratio of ~65% due to low earnings multiple being assigned to the company by the markets.

Safety, Quality, Competitive Advantage, & Recession Resiliency

: Still A Buy? 4")

Owens & Minor has experienced a deterioration in several of its quality metrics in the last several years. Most notably, its dividend payout ratio has increased and its interest coverage ratio has fallen (because of the $450 million of new debt it acquired to fund the Halyard Health acquisition). These metrics should improve over the next several years.

Owens & Minor’s competitive advantage comes from its entrenched position within the healthcare distribution industry and its strong relationships with customers. The company has a customer base of approximately 4,400 hospital systems and boasts an on-time delivery rate of 99%. Owens & Minor is also very recession-resistant. The company increased its adjusted earnings-per-share each year during the 2007-2009 financial crisis.

Final Thoughts & Recommendation

Owens & Minor’s expected total returns are some of the highest in our coverage universe, driven by its potential for valuation expansion and its high dividend yield. With that said, some of the company’s quality metrics have deteriorated in recent years. In particular, we find the company’s recent drop in interest coverage – driven by debt issued to fund acquisitions – to be somewhat troublesome. If these acquisitions can be integrated successfully and if the corresponding cash flows are used to pay down the associated debt, Owens & Minor’s stock should handsomely reward today’s investors over the next 5 years. The company’s strong total return potential combined with its leverage and recent poor operating performance make this stock a buy, but only for investors with a high risk tolerance.

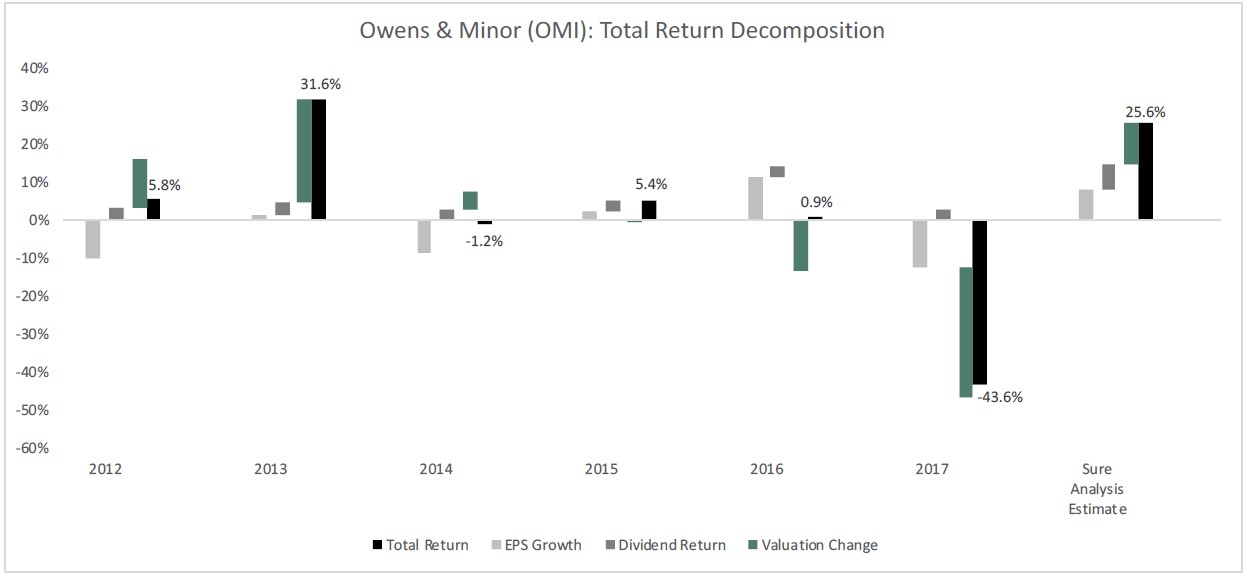

Total Return Breakdown by Year

: Still A Buy? 5")

Owens & Minor is a great example of a quality high dividend stock (its yield is well over 6%) that is undervalued and has solid growth potential.

For more stocks with the above characteristics try our Sure Retirement Newsletter, which features the top 10 securities with 4%+ yields each month. The next edition comes out this Sunday. Click here to start your risk-free 7 day trial now.

Thanks,

Ben Reynolds

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.